Estimate child care costs: The True Cost of High-Quality Child Care Across the United States

Provider Cost of Quality Calculator

View COVID-19 resources for CCDF Lead Agencies, providers, and families. Learn about provider eligibility for the COVID-19 vaccination.

Agency links

- U.S. Department of Health & Human Services

- Administration for Children & Families

- Office of Child Care (return to main site)

- OCC Technical Assistance Network

You are here

Home > Provider Cost of Quality Calculator

The Provider Cost of Quality Calculator (PCQC) helps you estimate the annual costs and revenue of operating a center or home-based child care program at different quality levels. This information can help owners and operators better understand the factors that influence costs and revenue and help the policy community design financial supports. Intended audiences include the following:

- State and territory Child Care and Development Fund Administrators and staff

- Policymakers

- Child care resource and referral agency staff

- Child care organizations and networks

- Owners and operators of child care centers and family child care homes

The following resources can help you use PCQC. They offer an overview of PCQC’s capabilities and include instructions to help you enter data.

Start Using the PCQC

*New!* Check out the updated PCQC! it features a streamlined design and a cost-per-child output, among other new features.

You can still access the legacy PCQC through this login page until December 30. Learn how to export and save your legacy PCQC scenarios before then by using this tipsheet.

Find Additional Information

*New!* User Guide for the Provider Cost of Quality Calculator explains how to use the updated PCQC.

- User Guide for the Provider Cost of Quality Calculator (February 2022)

This guide will tell you how to use the legacy PCQC—from the basics to calculations. - Using the PCQC to Estimate the Cost of Quality (July 2022)

Lead Agencies can use various strategies to support the child care system—this guide shows you how to use PCQC to understand these strategies’ fiscal impact.

- The New Normal: What Is the Impact on Provider Costs? (December 2020)

This one-pager explains how PCQC can help states, territories, and Tribes understand the costs of coronavirus disease 2019 (COVID-19) mitigation practices in early care and education settings—this resource can also inform design of financial support and incentive packages. - Increasing Quality in Early Care and Education Programs: Effects on Expenses and Revenues (November 2015)

The brief explains the effects of the following variables on provider financial health and viability—increased levels of quality, ratios and group sizes, and compensation increases. - Understanding the Potential of the Provider Cost of Quality Calculator (March 2015)

This presentation was part of the national webinar conducted in March 2015—it covers a brief history, capabilities, and a state example. - Early Care and Education Program Characteristics: Effects on Expenses and Revenues (November 2014)

This brief explains how the following variables affect provider financial health and viability—participation in the Child and Adult Care Food Program, program size and ages of children accepted into care, enrollment efficiency, and bad debt or uncollected revenues.

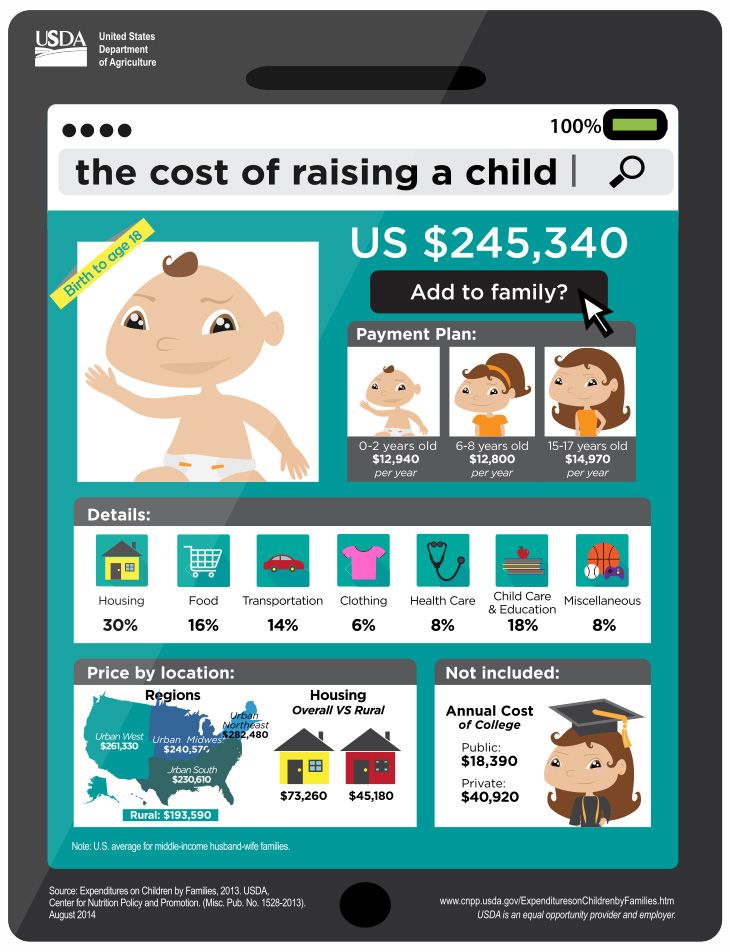

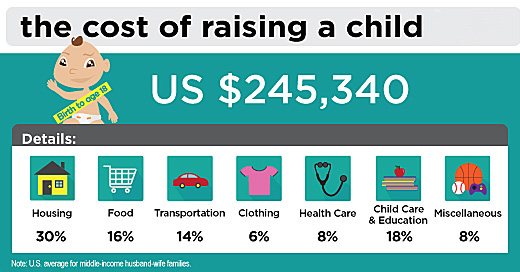

Child care costs in the United States

{{ active.infant_care_annual }}

Child care is one of the biggest expenses families face.

- {{#if active.infant_greater_tuition }}Infant care in {{ active.name }} costs {{ active.infant_tuition_dollar_difference }} ({{ active.infant_tuition_percent_difference }}) more per year than in-state tuition for four-year public college.{{ else }}Infant care in {{ active.name }} costs just {{ active.infant_tuition_dollar_difference }} ({{ active.infant_tuition_percent_difference }}) less than in-state tuition for four-year public college.{{/if}}{{#if active.infant_greater_tuition }}

- That makes {{ active.name }} one of 33 states and DC where infant care is more expensive than college.{{/if}}

- {{ active.rent_bullet_text }}.

Annual cost in {{ active.name }}

College: {{ active. college_cost }} college_cost }} |

|

|---|---|

| Housing: {{ active.rent_cost }} | |

| 4-year-old care: {{ active.four_care_annual }} | |

| Infant care: {{ active.infant_care_annual }} | |

Share this chart

<div><a href=”#share”><i></i></a><a data-foo=”tweet” href=”https://twitter.com/intent/tweet?text=https%3A%2F%2Fgo.epi.org%2FRS3+How+much+is+child+care+in+%7B%7B+active.name+%7D%7D%3F&url=https%3A%2F%2Fgo.epi.org%2FgxpJ”><i></i></a><a href=”http://www.epi.org/files/cc/bar/{{ active.id }}.png”><i></i></a><a href=”#” data-toggle2-target=”.chart-ext-info”><i></i></a><div><div><p>Copy the code below to embed this chart on your website. </p><textarea><iframe src=”https://www.epi.org/?page_id=102696&view=embed#/{{ active.id }}” frameborder=”0″></iframe></textarea><a href=”#”><i></i></a></div></div></div>

</p><textarea><iframe src=”https://www.epi.org/?page_id=102696&view=embed#/{{ active.id }}” frameborder=”0″></iframe></textarea><a href=”#”><i></i></a></div></div></div>

Child care is unaffordable for typical families in {{ active.name }}.

- Infant care for one child would take up {{ active.infant_share_med }} of a median family’s income in {{ active.name }}.

- According to the U.S. Department of Health and Human Services (HHS), child care is affordable if it costs no more than 7% of a family’s income. By this standard, only {{ active.infant_affordability }} of {{ active.name }} families can afford infant care.

Families with two children face an even larger burden.

- Child care for two children—an infant and a 4-year-old—costs {{ active.infant_four_annual }}. That’s {{ active. infant_four_rent_difference }} {{ active.infant_four_rent_greater }} than average rent in {{ active.name }}.

- A typical family in {{ active.name }} would have to spend {{ active.infant_four_share_median }} of its income on child care for an infant and a 4-year-old.

infant_four_rent_difference }} {{ active.infant_four_rent_greater }} than average rent in {{ active.name }}.

infant_four_rent_difference }} {{ active.infant_four_rent_greater }} than average rent in {{ active.name }}.Child care is out of reach for low-wage workers.

- A minimum wage worker in {{ active.name }} would need to work full time for {{ active.infant_cost_weeks }} weeks, or from January to {{ active.infant_cost_month }}, just to pay for child care for one infant. {{#if active.has_local_min_wage }}

- Even in {{ active.min_wage_locale }}, where the local minimum wage is the highest in the state (${{ active.min_wage_local_amount }}), it would take {{ active.infant_cost_weeks_local }} weeks to cover the costs.{{/if}}

Yet, child care workers still struggle to get by.

- Nationally, child care workers’ families are more than twice as likely to live in poverty as other workers’ families (11. 8% are in poverty compared with 5.8%).

- A median child care worker in {{ active.name }} would have to spend {{ active.infant_share_worker }} of her earnings to put her own child in infant care.

8% are in poverty compared with 5.8%).

8% are in poverty compared with 5.8%).How big a bite does child care take?

Infant care costs as a share of income in {{ active.name }}

HHS affordability standard: Child care should cost no more than 7% of a family’s income.

Share this chart

<div><a href=”#share”><i></i></a><a data-foo=”tweet” href=”https://twitter.com/intent/tweet?text=https%3A%2F%2Fgo.epi.org%2FqSW+How+much+is+child+care+in+%7B%7B+active.name+%7D%7D%3F&url=https%3A%2F%2Fgo.epi.org%2FgxpJ”><i></i></a><a href=”http://www.epi.org/files/cc/pie/{{ active.id }}.png”><i></i></a><a href=”#” data-toggle2-target=”.chart-ext-info”><i></i></a><div><div><p>Copy the code below to embed this chart on your website. </p><textarea><iframe src=”https://www.epi.org/?page_id=102483&view=embed#/{{ active.id }}” frameborder=”0″></iframe></textarea><a href=”#”><i></i></a></div></div></div>

</p><textarea><iframe src=”https://www.epi.org/?page_id=102483&view=embed#/{{ active.id }}” frameborder=”0″></iframe></textarea><a href=”#”><i></i></a></div></div></div>

Everyone will benefit if we solve this problem.

- Meaningful child care reform that capped families’ child care expenses at 7% of their income would save a typical {{ active.name }} family with an infant {{ active.infant_savings_to_family }} on child care costs. This would free up {{ active.infant_share_free_up }} of their (post–child care) annual income to spend on other necessities.

- Parents would have more opportunities to enter the labor force. If child care were capped at 7% of income, {{ active.additional_mothers }} more parents would have the option to work.

- This reform would expand {{ active.name }}’s economy by {{ active.state_gsp_percent }}. That’s {{ active. state_gsp_text }} of new economic activity.

state_gsp_text }} of new economic activity.

state_gsp_text }} of new economic activity.How does your state stack up?

Share this chart

<div><a href=”#share”><i></i></a><a data-foo=”tweet” href=”https://twitter.com/intent/tweet?text=https%3A%2F%2Fgo.epi.org%2FFq1+How+much+is+child+care+in+your+state%3F&url=https%3A%2F%2Fgo.epi.org%2FgxpJ”><i></i></a><a href=”http://www.epi.org/files/cc/map.png”><i></i></a><a href=”#” data-toggle2-target=”.chart-ext-info”><i></i></a><div><div><p>Copy the code below to embed this chart on your website.</p><textarea><iframe src=”https://www.epi.org/?page_id=102695&view=embed#/{{ active.id }}” frameborder=”0″></iframe></textarea><a href=”#”><i></i></a></div></div></div>

David Blau, The Child Care Problem: An Economic Analysis, Russell Sage Foundation, 2001.

Bureau of Economic Analysis, GDP and Personal Income Regional Economic Accounts [Interactive data tables], 2017.

Bureau of Labor Statistics, Occupational Employment and Wage Estimates, May 2018.

Child Care Aware of America, The U.S. and the High Cost of Child Care: A Review of Prices and Proposed Solutions for a Broken System, 2018.

Department of Health and Human Services, Child Care and Development Fund (CCDF) Program; Proposed Rule, 80 Fed. Reg. 80466–80582 (December 24, 2015).

Economic Policy Institute, Current Population Survey Extracts, version 0.6.0., 2019.

U.S. Census Bureau, American Community Survey, “Median Gross Rent: ACS 5-year Estimates for 2013–2017” [online data table], 2018.

U.S. Department of Education, National Center for Education Statistics, “Table 330.20. Average Undergraduate Tuition and Fees and Room and Board Rates Charged for Full-time Students in Degree-Granting Postsecondary Institutions, by Control and Level of Institution and State or Jurisdiction” [online data table], 2018.

Children’s budget

- 2021

- 2020

- 2019

- References

-

Infographics for all regions

Rating of subjects of the Russian Federation by social spending on children

Social spending on children by regions of the Russian Federation

Map of social spending on children by regions of the Russian Federation (general) 9017

014 Map of spending on children’s education by regions of the Russian Federation

Map of spending on children’s healthcare by regions of the Russian Federation

Map of spending on social support for children by regions of the Russian Federation

Map of spending on children in terms of supporting active employment by regions RF

Map of expenses for children in the field of culture by regions of the Russian Federation

Map of expenses for children in the field of physical culture and sports by regions of the Russian Federation

Map of spending on youth policy by regions of the Russian Federation

-

Infographics for all regions

Total expenditures on children of the consolidated budgets of the constituent entities of the Russian Federation

Regional budget expenditures on children in the framework of the implementation of national projects

0014 Expenses of regional budgets for children by certain categories of recipients

-

Total expenses for children of the consolidated budgets of the subjects of the Russian Federation

Expenses of regional budgets for children in the framework of the implementation of national projects

Expenditures of regional budgets for children in the framework of the implementation of the Decade of Childhood

Expenses of regional budgets for children by certain categories recipients

-

Foreign experience in the formation of the children’s budget

“Children’s budget” is the cost of the state for children, their health, education, cultural and physical development, including for children who, for various reasons, were left without parental care, the cost of social support for families during the birth and upbringing of children , support for motherhood and fertility.

In 2020, specialists from the NIFI, the Department of Budget Policy in the Sphere of Labor and Social Protection of the Russian Ministry of Finance (Department) and financial authorities worked to form the so-called “Children’s Budget” of the country. If until that time the Department formed the federal “Children’s Budget”, then this year the structure and methodology for collecting the necessary data from the “Children’s Budget” at the regional level was developed. As a result, a full-fledged document was formed, which collected the maximum possible data on the expenditures of regions and municipalities on state support for families and children.

This work is not the first attempt to create such a document. In the mid-2000s, the experiment was conducted in Moscow, and today – in a number of regions (St. Petersburg, the Republic of Karelia, Volgograd, Moscow, Smolensk, Ivanovo and Chelyabinsk regions), the laws on regional budgets already contain an analytical section, which presents data on budget expenditures for childhood.

The regions have different approaches to the formation of the children’s budget.

Ivanovo region presents expenditures broken down by government programs, subprograms, regional projects and major events. At the same time, both regional and federal funds are indicated.

The Volgograd region generates expenses for childhood in 10 tables by areas: in the field of transport services; in the field of providing citizens with affordable and comfortable housing; in the field of construction; in the field of employment of the population; in the health sector; in the field of culture; in the field of mass media; in the field of physical culture and sports; in the field of social support of the population; in education and youth policy. Inside, for each area, directions for spending budget funds (specific measures) and the category of recipients of these funds (individuals, subordinate institutions, organizations implementing these measures) are indicated.

The Moscow region uses a departmental classification of budget expenditures by sections, subsections and target items (state programs, subprograms and main events).

The Republic of Karelia presents data broken down by state programs, subprograms, main activities and activities (types of expenditure). The Smolensk region presents the same data within the framework of the functional classification. And the Chelyabinsk region – in the context of state programs, subprograms, events, but indicating only targeted articles.

The federal “Children’s budget” is formed in the program and non-program part of the costs. The program part reflects the costs of the state program and specific activities. The non-programme part of the expenditures is presented in the context of the expenditures of state bodies on ensuring the activities (rendering of services) of state institutions (for example, general education) and social support for their employees.

All approaches have a right to exist, but they (except the federal one) are absolutely understandable only to those who form and approve the budget (since they are formed in terms and rules of the budget, this is very convenient), but in most cases they are completely incomprehensible to other citizens.

The format, which was developed by the Ministry of Finance of Russia and NIFI, was maximally (as far as possible) adapted to the presentation of the “Children’s Budget” to the general public.

Information on the amount of budgetary appropriations of the consolidated budget of the constituent entities of the Russian Federation directed to state support for families and children is presented in the form of four tables.

Table No. 1 ( 2019 ., 2020 ) “Information on the volume of budgetary appropriations of the consolidated budget of the constituent entity of the Russian Federation allocated to state support for families and children” is a summary table that presents data in general for the entire “Children’s Budget” The remaining tables reflect the same expenses in different sections (important for deputies).

Table No. 2 ( 2019 ., 2020 ) “Report on the participation of the constituent entity of the Russian Federation in the implementation of national projects and on plans for participation in the implementation of national projects in the current and subsequent periods in terms of the implementation of activities aimed at supporting children and families with children (consolidated budget of a constituent entity of the Russian Federation).

Table No. 3 ( 2019 , 2020 ) “Report on the expenditures of the consolidated budget of the subject of the Russian Federation for the implementation of the Action Plan for the implementation of the Decade of Childhood (Approved by the decision of the Government of the Russian Federation of July 6, 2018 No. 1375-r) (in terms of activities, the number of responsible executors of which includes the subjects of the Russian Federation)”.

Table No. 4 ( 2019 ., 2020 ) “Information on the volume of budgetary appropriations of the consolidated budget of the constituent entity of the Russian Federation allocated for payments and benefits provided to certain categories of recipients.”

The tables include information on the expenditures of the subject of the Russian Federation and the budgets of municipalities allocated for state support of families and children. Thus, almost all state expenses are subject to accounting, since the federal and even more so regional budgets are not formed in the context of individual services and activities. It is practically impossible to isolate the expenses that go specifically to the family and children, for example, in a city clinic, hospital, library, sports complex or theater, unless these are specialized children’s institutions. In this regard, of course, a certain amount of conventionality in the generated data will be present. In order to solve this problem, it will be necessary to make significant changes to the budget classification.

It is practically impossible to isolate the expenses that go specifically to the family and children, for example, in a city clinic, hospital, library, sports complex or theater, unless these are specialized children’s institutions. In this regard, of course, a certain amount of conventionality in the generated data will be present. In order to solve this problem, it will be necessary to make significant changes to the budget classification.

Education measures included expenses for pre-school, general, vocational and additional education, as well as expenses for social support measures administered by educational authorities – school meals (hot meals) and reimbursement of parental fees for childcare and care.

In terms of health care measures, only those expenses incurred by the consolidated budget of the region for the maintenance and development of state and municipal medical organizations (institutions) providing services to families with children and children were taken into account, that is, without taking into account compulsory medical insurance funds. It also presents the costs of social support measures that are administered by the health authorities – drug provision of children, vaccination of children, provision of special and dairy products for children under 3 years of age, pregnant women and nursing mothers, provision of families with newborn children with gift sets of children’s accessories.

It also presents the costs of social support measures that are administered by the health authorities – drug provision of children, vaccination of children, provision of special and dairy products for children under 3 years of age, pregnant women and nursing mothers, provision of families with newborn children with gift sets of children’s accessories.

To assess the costs of social support for children and families with children, a list of social support measures was used, which is the same for all regions. Costs for measures that are specific to the region were included in the general line. In addition, the costs of maintaining and developing social service institutions and organizations that provide certain services to children and families with children were subject to assessment.

Expenses for orphans and children left without parental care, in particular, the volume of financial support for educational organizations for orphans, medical organizations for orphans and organizations providing social services for orphans, are subject to a separate assessment. In addition, data was collected on key areas of social support:

In addition, data was collected on key areas of social support:

a) payments (allowances, compensations, scholarships, etc.) and in-kind assistance to orphans and children left without parental care;

b) payments (allowances, compensations, etc.) and assistance in kind to guardians, trustees, foster parents, adoptive parents;

c) providing housing for orphans and persons from among orphans and children left without parental care.

Also, special attention was paid to the costs of the implementation of activities, payments and benefits provided to specific categories of recipients, such as: large families, young families, disabled children and families with children with disabilities or children with disabilities, students and student families , low-income families, families with children who do not have preferential status, which reflects approaches to the amount of funding for certain areas of state policy (Table 4 of the “Children’s Budget”).

Comparative analysis of data on the “children’s budget” among the regions in 2020

for state support for families and children.

Figure 1 – Spending by the constituent entities of the Russian Federation on state support for families and children in 2020

Figure 2 – Examples of the structure of expenditures of constituent entities of the Russian Federation on state support for families and children in 2020

Source: Calculated by the authors based on the data provided by the constituent entities of the Russian Federation to the Ministry of Finance of Russia as part of the “Information on the volume of budget allocations of the consolidated budget of the constituent entities of the Russian Federation allocated to state support for families and children.”

Figure 3 – Spending by the constituent entities of the Russian Federation on state support for families and children in 2020: education

Source: Calculated by the authors based on the data provided by the constituent entities of the Russian Federation to the Ministry of Finance of Russia as part of the “Information on the volume of budget allocations of the consolidated budget of the constituent entities of the Russian Federation directed to state support for families and children. ”

”

Figure 4 – Spending by the constituent entities of the Russian Federation on state support for families and children in 2020: health care

Source: Calculated by the authors based on the data submitted by the constituent entities of the Russian Federation to the Ministry of Finance of Russia as part of the “Information on the volume of budget allocations of the consolidated budget of the constituent entities of the Russian Federation directed to state support for families and children.”

Figure 5 – Spending by the constituent entities of the Russian Federation on state support for families and children in 2020: social support for the population

appropriations of the consolidated budget of the constituent entities of the Russian Federation allocated for state support of families and children.

Figure 6 – the expenses of the constituent entities of the Russian Federation for state support for families and children in 2020: Active employment policy

Source: calculated by the authors according to the subjects of the Russian Federation to the Ministry of Finance of Russia as part of “Information on the volumes of budgetary assistance of consolidated the budget of the constituent entities of the Russian Federation allocated for state support of families and children.

Figure 7 – Spending by the constituent entities of the Russian Federation on state support for families and children in 2020: culture

the budget of the constituent entities of the Russian Federation allocated for state support of families and children.

Figure 8 – Spending by the constituent entities of the Russian Federation on state support for families and children in 2020: physical culture and sports

Figure 9 – Spending by the constituent entities of the Russian Federation on state support for families and children in 2020: youth policy

Source: Calculated by the authors based on the data provided by the constituent entities of the Russian Federation to the Ministry of Finance of Russia as part of the “Information on the volume of budgetary appropriations of the consolidated budget of the constituent entities of the Russian Federation directed to state support for families and children. ”

”

Figure 10 – Spending by the constituent entities of the Russian Federation on state support for families and children in 2020: support for orphans

|

Is it possible to include the cost of utility bills in the parental fee for supervision and care in a municipal preschool educational institution? Are utilities included in the concept of “maintenance of buildings”? Anna Alexandrovna Vavilova According to Part 2 of Art. 65 of the Federal Law “On Education in the Russian Federation” for the care and care of a child, the founder of an organization engaged in educational activities has the right to establish a fee charged from parents (legal representatives) (parental fee), and its amount, unless otherwise established by the Federal Law. The concept of “maintenance of the building”, and, consequently, the possible range of costs for the maintenance of the building, are determined on the basis of such a document as “Housing and communal services. Terms and Definitions. GOST R 51929-2002” (approved by the Decree of the State Standard of Russia dated August 20, 2002 No. 307-st). The specified GOST gives the following definition of building maintenance: “… Building maintenance [structures, equipment, communications, housing and communal facilities]: a range of services for maintenance, cleaning, diagnostics, testing and inspection of the building [structures, equipment, communications, facilities for housing and communal purposes] and technical supervision of its condition . However, this does not mean that these costs can be included in the cost of care and maintenance services in full. In its structure, the parental fee contains amounts intended to cover the expenses of an educational organization for the care and supervision of a child, including other expenses, incl. for the implementation of the educational program, for the maintenance of property, etc., is not allowed. At the same time, the supervision and care of a child is clearly defined by Article 2 of Federal Law No. 273-FZ as “a set of measures to organize nutrition and household services for children, ensure their personal hygiene and daily routine.” Accordingly, the law also limits the costs of care and maintenance to the costs of implementing this set of measures (and not any other measures). At the same time, it is necessary to assess what expenses should be included in the costs of catering, household services, personal hygiene and daily routine. This set of measures for its implementation requires, among other things, certain utility costs. By analogy, we can consider the composition of the costs of the service for the implementation of the educational program. In such a document as methodological recommendations for calculating the standard costs for the provision of services by a federal autonomous institution (performance of work), approved by order of the Ministry of Education and Science of the Russian Federation of June 3, 2010 No. 581, the cost standard for the provision of a unit of state educational service is included in the cost standard for utilities and other costs associated with the use of property, with the exception of semi-fixed costs for the maintenance of property, which are determined on the basis of the order of the Ministry of Economic Development of the Russian Federation dated April 17, 2009No. Thus, if property is used in the provision of care and maintenance services, which is also used in the process of implementing an educational program, then the founder takes into account the costs of maintaining such property when forming a subsidy for the implementation of a state (municipal) task. Consequently, part of the utility costs are already included in the standard costs for the maintenance of property, as well as in the standard costs for the provision of educational services under the preschool education program. |

At the same time, according to part 4 of this article, it is not allowed to include the costs of implementing the educational program of preschool education, as well as the costs of maintaining real estate of state and municipal educational organizations implementing the educational program of preschool education, in the parental fee for looking after and caring for a child in such organizations .

At the same time, according to part 4 of this article, it is not allowed to include the costs of implementing the educational program of preschool education, as well as the costs of maintaining real estate of state and municipal educational organizations implementing the educational program of preschool education, in the parental fee for looking after and caring for a child in such organizations .  .. “. Based on this definition, from a formal point of view, the costs of supplying electrical energy, drinking water, gas, thermal energy and hot water are not included in the cost of maintaining the building, and therefore, Federal Law No. 273-FZ does not directly prohibit including them in the parent fee.

.. “. Based on this definition, from a formal point of view, the costs of supplying electrical energy, drinking water, gas, thermal energy and hot water are not included in the cost of maintaining the building, and therefore, Federal Law No. 273-FZ does not directly prohibit including them in the parent fee.

134 “On Approval of Guidelines for the Calculation of Regulatory Costs for the Maintenance of Real Estate and Especially Valuable Movable Property Assigned to a Federal Autonomous Institution or Acquired by a Federal Autonomous Institution at the expense of funds allocated to it by the founder for the acquisition of such property (with the exception of property leased with the consent of the founder), as well as for the payment of taxes, for which the relevant property, including land plots, is recognized as taxation” and are taken into account as part of the standard costs for maintaining the property (and not the standard costs for the educational service).

134 “On Approval of Guidelines for the Calculation of Regulatory Costs for the Maintenance of Real Estate and Especially Valuable Movable Property Assigned to a Federal Autonomous Institution or Acquired by a Federal Autonomous Institution at the expense of funds allocated to it by the founder for the acquisition of such property (with the exception of property leased with the consent of the founder), as well as for the payment of taxes, for which the relevant property, including land plots, is recognized as taxation” and are taken into account as part of the standard costs for maintaining the property (and not the standard costs for the educational service).