Kindercare payroll: Corporate Contact Information | KinderCare

Working At KinderCare Education: Employee Reviews and Culture

The Culture At KinderCare Education

Information provided by the company

Hardworking and professional, yet relaxed and fun, our Corporate Accounting and Payroll team unite to positively impact the lives of our employees and our KinderCare Education families. When you join our team as a Sr.

At KinderCare Education, we make it our passion to nurture a sense of discovery, joy, and wonder in every child, every day, at every one of our centers.

Do you have a passion for working with children

Leverage your business, sales and marketing savvy to grow KinderCare Education’s presence in the community, leading to the growth of new families and children in our centers.

Whether you’re in one of our centers or providing support from our headquarters in Portland, Oregon, being a part of the KinderCare family means that you care deeply about positively impacting the lives of children and families through the power of education.

Show More

KinderCare Education Overview

Website

www.kindercare.com

Organization Type

Education

The Team At KinderCare Education

KinderCare Education Company Rankings

KinderCare Education is ranked #97 on the Best Companies to Work For in Oregon list. Zippia’s Best Places to Work lists provide unbiased, data-based evaluations of companies. Rankings are based on government and proprietary data on salaries, company financial health, and employee diversity.

- #97 in Best Companies to Work For in Oregon

- #5 in Best Education Companies to Work For in Oregon

- #2 in Best Education Companies to Work For in Portland, OR

- #2 in Biggest Companies in Oregon

- #1 in Biggest Companies in Portland, OR

Read more about how we rank companies.

KinderCare Education Salaries

Highest Paying Jobs At KinderCare Education

| Rank | Job Title | Avg. Salary Salary |

Hourly Rate |

|---|---|---|---|

| 1 | Center Director | $45,926 | $22 |

| 2 | Teacher | $36,140 | $17 |

| 3 | Assistant Director | $35,560 | $17 |

| 4 | Programming Specialist | $31,432 | $15 |

| 5 | Teaching Assistant | $30,420 | $15 |

| 6 | Bus Driver | $29,257 | $14 |

| 7 | Floater | $28,101 | $14 |

| 8 | Child Care Worker | $27,597 | $13 |

| 9 | In-Home Childcare Provider | $27,480 | $13 |

| 10 | Cook | $27,351 | $13 |

9.5

Diversity Score

We calculated the diversity score of companies by measuring multiple factors, including the ethnic background, gender identity, and language skills of their workforce.

KinderCare Education Gender Distribution

Female

Research Summary. Using a database of 30 million profiles, Zippia estimates demographics and statistics for KinderCare Education. Our estimates are verified against BLS, Census, and current job openings data for accuracy. After extensive research and analysis, Zippia’s data science team found that:

-

KinderCare Education has 36,000 employees.

-

87% of KinderCare Education employees are women, while 13% are men.

-

The most common ethnicity at KinderCare Education is White (66%), followed by Hispanic or Latino (14%) and Black or African American (11%).

-

KinderCare Education employees are most likely to be members of the democratic party.

-

On average, employees at KinderCare Education stay with the company for 3.8 years.

-

The average employee at KinderCare Education makes $31,241 per year.

Biggest KinderCare Education Locations

| Rank | City | Job Count |

|---|---|---|

| 1 | Phoenix, AZ | 32 |

| 2 | San Diego, CA | 27 |

| 3 | New York, NY | 25 |

| 4 | Houston, TX | 19 |

| 5 | Austin, TX | 16 |

| 6 | San Jose, CA | 15 |

| 7 | Chicago, IL | 14 |

| 8 | Philadelphia, PA | 14 |

| 9 | Dallas, TX | 11 |

| 10 | Los Angeles, CA | 6 |

Jobs from companies you might like

Do you Work At KinderCare Education?

Help us make this company more transparent.

KinderCare Education Employee Political Affiliation

KinderCare Education employees are most likely to be members of the Democratic Party.

The largest donation made to a political party by a KinderCare Education employee was

by Keith Lundquist. Keith Lundquist donated

$1,555 to the Republican Party.

Parties

Democratic Party

77.3 %

–

Republican Party

22.7 %

–

Employee Political Donations

| Name | Job Title | Party | Donation |

|---|---|---|---|

| Keith Lundquist | Teacher | Republican Party | $1,555 |

| Celia Sims | Vice President | Republican Party | $1,500 |

| Stacey Iverson | Teacher | Democratic Party | $1,009 |

| Ray Nelson | Teacher | Democratic Party | $800 |

| Sharon Russell | Child Care Director | Republican Party | $518 |

| Barb Otterness | Teacher | Republican Party | $505 |

| Cheryl Shelton | Center Director | Republican Party | $450 |

| Joshua Hornick | Finance Professional | Democratic Party | $450 |

| Mary Maloney | Finance Professional | Democratic Party | $350 |

| Randall Zeller | Finance Professional | Democratic Party | $300 |

Show More

KinderCare Education Employment Videos

Our Educators Are Our Heroes! Become a Part of the KinderCare Education Story. (It’s a Great One!)

(It’s a Great One!)

How Would You Rate The Company Culture Of KinderCare Education?

Have you worked at KinderCare Education? Help other job seekers by rating KinderCare Education.

KinderCare Education Subsidiaries

Subsidiaries to KinderCare Education include Children’s Creative Learning Center, Inc.. Employees at the parent organization, KinderCare Education, earn $31,241 whereas employees at Children’s Creative Learning Center, Inc. earn $38,378, on average.

Children’s Creative Learning Center, Inc.

Salary Range27k – 53k$38k$38,378

$27k

$53k

Frequently Asked Questions about KinderCare Education

When was KinderCare Education founded?

KinderCare Education was founded in 1969.

How many Employees does KinderCare Education have?

KinderCare Education has 36,000 employees.

How much money does KinderCare Education make?

KinderCare Education generates $7. 8B in revenue.

8B in revenue.

What industry is KinderCare Education in?

KinderCare Education is in the education management industry.

What is KinderCare Education’s mission?

KinderCare Education’s mission statement is “KinderCare Education is rooted in a profound respect for children, and providing them with the very best start in life is our purpose and our mission.”

What type of company is KinderCare Education?

KinderCare Education is a education company.

Who are KinderCare Education’s competitors?

KinderCare Education competitors include Bright Horizons, Childtime, Goddard School, Childcare Network, Kids ‘R’ Kids, The Learning Experience, Tutor Time, Children of America, Children’s Learning Center, The Children’s Courtyard, Minnieland Academy, Brightside Academy, Rainbow Child Development Center, Child Development Center, Sunrise Preschools, Headstart, New Horizon Academy, Creative Kids Learning Center, Preschool Of The Arts, Discovery Point.

Who works at KinderCare Education?

Tom Wyatt (Chief Executive Officer)

Perry Mendel (Founder)

Are You An Executive, HR Leader, Or Brand Manager At KinderCare Education?

Claiming and updating your company profile on Zippia is free and easy.

Zippia gives an in-depth look into the details of KinderCare Education, including salaries, political affiliations, employee data, and more, in order to inform job seekers about KinderCare Education. The employee data is based on information from people who have self-reported their past or current employments at KinderCare Education. The data on this page is also based on data sources collected from public and open data sources on the Internet and other locations, as well as proprietary data we licensed from other companies. Sources of data may include, but are not limited to, the BLS, company filings, estimates based on those filings, h2B filings, and other public and private datasets. While we have made attempts to ensure that the information displayed are correct, Zippia is not responsible for any errors or omissions or for the results obtained from the use of this information. None of the information on this page has been provided or approved by KinderCare Education. The data presented on this page does not represent the view of KinderCare Education and its employees or that of Zippia.

While we have made attempts to ensure that the information displayed are correct, Zippia is not responsible for any errors or omissions or for the results obtained from the use of this information. None of the information on this page has been provided or approved by KinderCare Education. The data presented on this page does not represent the view of KinderCare Education and its employees or that of Zippia.

KinderCare Education may also be known as or be related to KinderCare Education, KinderCare Learning Companies Inc, KinderCare Education LLC, Kindercare, KinderCare Learning Centers, KinderCare Learning Centers LLC and Kindercare Education LLC.

Day-care centers struggle to rehire, worry many have left the industry

A sign sits in front of the KinderCare Learning Center on February 5, 2015 in Palatine, Illinois.

Scott Olson | Getty Images News | Getty Images

Angela Garcia has about a dozen open positions at her two child-care centers in New Mexico. She’s tried job fairs, sign-on bonuses, retention incentives and working with recruiters to fill the openings, but nothing has worked.

She’s tried job fairs, sign-on bonuses, retention incentives and working with recruiters to fill the openings, but nothing has worked.

By her count, between five and eight of those jobs have been open for more than six months. One week, Garcia had 12 job interviews scheduled, but only three of the applicants showed up. When she offered positions to two of them, they both turned her down.

“I’ll be completely honest, we are at a loss,” said Garcia. “We are not having any luck finding anyone that wants to return to the workforce at this point. If we don’t begin to get staff into our centers, I’m potentially looking at closing classrooms, which is only going to decrease access to my families, and I’m not really sure how that’s going to help our community recover.”

Garcia’s child-care center isn’t alone in facing this problem. Around the country, day-care centers and summer camps are struggling to operate at full capacity due to widespread worker shortages. The problem has resulted in waiting lists for parents looking for child care. With many companies aiming to bring staff who worked from home during the Covid pandemic back into the office this fall, the problem could worsen because the demand for care will grow. And without child care, other parents may have to step out of the workforce, slowing the economic recovery.

With many companies aiming to bring staff who worked from home during the Covid pandemic back into the office this fall, the problem could worsen because the demand for care will grow. And without child care, other parents may have to step out of the workforce, slowing the economic recovery.

A camp in New Hampshire was forced to close its doors because of staff and food shortages. According to a report by The Boston Globe last week, as training was set to begin, the camp’s owners were still looking to hire as many as 20 counselors after earlier hires disappeared.

Employers in the child-care industry have long struggled to find, hire and retain skilled workers, but this is a problem that was made worse by the pandemic. The industry lost about 350,000 child-care workers — about a third of its workforce — during the health crisis due to layoffs and it hasn’t yet been able to recoup these losses, said Cindy Lehnhoff, director of the National Child Care Association. Even centers that kept their doors open last year have lost staff as many were unwilling or unable to work through the pandemic.

Annual turnover in the industry pre-pandemic has been estimated to be as high as 30%, according to Katie Hamm, associate deputy assistant secretary for early childhood development at the Administration for Children and Families, part of the Department of Health and Human Services. Churn can hurt the quality of care children receive, she said.

‘A quiet crisis’ worsens

“At the height of the pandemic, we lost a lot of early childhood educators. Since President Biden took office in 2020, we’ve added about 65,000 child-care jobs. That puts us at 89% of the pre-pandemic level, but definitely not enough,” Hamm said.

“Across the board, there is difficulty in hiring folks in the early childhood sector,” Hamm said. “We had kind of a quiet crisis before the pandemic in the sector. And now that’s … really coming to the forefront.”

National child-care provider KinderCare has hired 11,500 teachers this year, according to CEO Tom Wyatt. The company has about 3,300 open teaching positions and plans to hire 5,200 more when schools open in the fall.

KinderCare has been able to attract workers because of its culture and the benefits it offers employees, which include health insurance, a 401(k) plan, child-care discounts, and reimbursements for degrees and certifications, Wyatt said. As a national company, KinderCare has the benefit of scale that many smaller providers don’t, he said. But even with these advantages, the company isn’t operating at full capacity.

“We are at least 25% to 30% higher than minimum wage in every market, and really much higher than that in most markets,” Wyatt said. “We raise our teacher salaries every year. … But to think that we would be able to raise tuition rates to a point to get teachers to even a further livable wage is hard for me to see right now.”

The vast majority of child-care providers in the U.S., 93%, are small businesses, and many lack the budget to raise salaries because the businesses are already operating on small profit margins, said Lehnhoff, who has worked in the industry for years.

“If we want to get America back to work, we’re going to have to recognize that child care and early education at a higher quality level is a business that is essential,” said Lehnhoff. “Child care is at a point they can’t charge anymore to middle America, which means they can’t raise their wages.”

She said she has seen many workers struggle to survive on low wages, even if benefits are available to them.

“They could not afford the benefits, even though we had a variety of packages, even wellness, because they needed the money they earned to live on. So benefits is not the biggest concern in the industry. It’s just there’s not a living wage,” said Lehnhoff.

Experts and employers agree that the industry’s staffing crisis is driven by poor compensation for its workers. According to Hamm, the national average wage is $12 an hour.

Parents wait for classrooms to open

Salaries at Garcia’s center range from $10.50 per hour up to $25 per hour depending on experience and if the worker has a college degree. Her centers stayed open during the pandemic and none of her workers were laid off. However, 12 staffers quit within the first three months of the crisis. Garcia reached out to those workers whenever the centers had more demand, but they either did not respond or said they didn’t want to work through the pandemic.

Her centers stayed open during the pandemic and none of her workers were laid off. However, 12 staffers quit within the first three months of the crisis. Garcia reached out to those workers whenever the centers had more demand, but they either did not respond or said they didn’t want to work through the pandemic.

At full capacity, Garcia needs 60 to 70 employees to care for around 300 children. Now she only has 40 workers and is forced to leave a classroom closed since she can’t staff it.

In order to service all the families on her waitlist, Garcia needs to hire 12 workers as soon as possible. But 20 hires, who fall under every level of qualification, would get her business open at full capacity, offering care seven days a week.

High turnover was not a problem for Garcia before the pandemic because of the 20-year relationship she had built with the staff at one of her centers. This was not the case at her second location, which she opened in October 2019, because she was still building a team when the pandemic hit. Now, Garcia is having a hard time at both locations.

Now, Garcia is having a hard time at both locations.

Garcia, who is the president of a child-care association in New Mexico, said she is hearing from providers all over the state who are having similar employment issues, especially those in rural areas. Around 200 centers, which represented 20% of those in the state, closed in the last year, Garcia said. About 900 people are claiming unemployment in the early childhood education industry in the state, she said.

“It is impossible to provide quality care, safe programs, without a full staff, and we are the key to recovery. Our economy does not survive if families can’t go back to work, and families can’t go back to work if they don’t have access,” Garcia said. “We can’t provide access if we don’t have a full staff.”

To Garcia, the pandemic has caused an employment crisis in the child-care industry. She said she understands the fears people have about the risks of working through the pandemic.

Last year, KinderCare put around 31,000 employees, most of whom were teachers, on furlough after temporarily closing the majority of its centers except those that serviced essential workers, Wyatt said. He estimates the company lost 20% to 30% of those teachers.

He estimates the company lost 20% to 30% of those teachers.

“That can be for many reasons, they could be that they chose to go into another field, it could be that they have preexisting conditions, and they don’t want to come back to the classroom,” Wyatt said. “I think it’s more reluctance to come back to a classroom, a closed environment.”

KinderCare said it has been especially hard to find highly skilled workers. Currently, 5% to 8% of its classrooms are closed due to a lack of teachers.

“The demand for teachers is much higher than the number of teachers that are actually applying for work,” Wyatt said. “We have had challenges prior to Covid and we will continue to have challenges with turnover and the need for more teachers.”

Since candidates with the right skills and experience are scarce, KinderCare has been hiring workers with various levels of experience and training them.

Bright Horizons, which also owns and manages centers around the country, has been struggling to hire and hold on to staff as well. Demand for its services has been rising as Bright Horizon’s corporate clients sweeten child-care benefits for their workers.

Demand for its services has been rising as Bright Horizon’s corporate clients sweeten child-care benefits for their workers.

“We are really doing everything we can to attract employees,” said Maribeth Bearfield, chief human resources officer at Bright Horizons.

Delta variant fans safety fears

While wages and training help, workers also need to feel safe. Industry insiders said health precautions are being taken to protect workers from the virus, but many remain concerned it will spread in classrooms filled with children not yet eligible for vaccines. The delta variant, and reports of breakthrough infections, have fanned these fears. It also could pose a higher risk for vulnerable people or those who care for high-risk individuals.

Despite a lot being done to provide aid to the sector, Hamm said there is still systemic concerns that need to be addressed including lack of reliable wages and benefits to create working conditions that compare with other industries that require the same amount of training.

“We don’t necessarily have the working conditions that a lot of workers are looking for,” Hamm said. “We’re going to need major reform to make this better. The conditions that existed before the pandemic in the workforce have not been addressed.”

Supporting the industry

Industry insiders and the Biden administration have said the government needs to play a bigger role when it comes to child care, which has gotten expensive for parents and providers alike. Parents cannot afford the tuition that would make a worker’s wages and benefits attractive enough.

The Biden administration has said that employment issues and lack of access to child care stem from years of underinvestment, which the president plans to reverse with $450 billion in proposed spending as part of his American Families Plan. Of that, $225 billion will be dedicated to child-care cost subsidies. The plan aims to make sure families are paying no more than 7% of their income for child-care costs while workers get payed a minimum wage of $15 per hour.

Last week, the Biden administration unveiled a separate 10-year, $755 billion investment plan that includes funding that would expand child care for children up to 5 years old and improve pay and prospects for people who work in the caregiving industry, which includes child and elder care.

“You don’t want to increase costs for parents and you don’t want to undercut wages for providers, so that means you really need robust public funding to make sure you can do both of those things,” Hamm said.

The American Rescue Plan, which became law in March, included $39 billion for child care — the largest ever investments made in the sector, according to Hamm. People in the industry say that even though many centers closed, others were able to keep their doors open largely due to government aid.

Garcia said government aid is the reason why her business survived, but she worries about the future.

“Right now, I’m very thankful to say that I’m not on the brink of closure in the sense of finances. But what I do worry about is that as I began to possibly close classrooms, I will no longer be able to support the payroll that I currently have,” Garcia said.

But what I do worry about is that as I began to possibly close classrooms, I will no longer be able to support the payroll that I currently have,” Garcia said.

watch now

KinderCare Customer Service Phone Number (888) 525-2780, Email, Help Center

KinderCare Phone Numbers and Emails

Toll-Free Number:

-

(888) 525-2780

Customer Service:

-

(503) 872-1300 -

(800) 214-1607 -

(844) 889-4478

Accounting/ Billing:

-

(877) 778-2090

Headquarters:

-

(800) 633-1488

Legal:

-

(833) 523-7748Privacy Inquiries

KinderCare Emails:

Customer Service

General Info

Acquisitions team

Legal

Privacy Inquiries

Media

Sales/ Reservations

Procurement Department

More phone numbers and emails

Less phone numbers and emails

KinderCare Contact Information

KinderCare Website:

-

www. kindercare.com

kindercare.com

kindercare.com

kindercare.com KinderCare Help Center:

-

Visit contact page

Corporate Office Address:

KinderCare Learning Centers LLC

650 Holladay Street, Suite 1400

Portland,

Oregon

97232

United States

Other Info (opening hours):

Inquiring Families Hours:

Monday – Friday: 5:00 am- 8:00 pm (PST)

Saturday – Sunday: 9:00 am- 6:00 pm (PST)

Enrolled Families Hours:

Monday – Friday: 8:00 am-3:00 pm (PST)

Edit Business Info

KinderCare Rating Based on 144 Reviews

Rating details

1. 8

8

more details

Product or Service Quality

Customer service

Price Affordability

Website

Rating Details

Product or Service Quality

Customer service

Price Affordability

Website

Location

Diversity of Products or Services

Quality of Food

Value for money

Close

All 410 KinderCare reviews

Summary of KinderCare Customer Service Calls

Top Reasons of Customers Calls

Why Do People Call KinderCare Customer Service?

Employment Question:

-

“Trying to get my job back”

-

“Need a copy of my check stub”

-

“401k question”

Request for Information Question:

-

“I would like to know if my direct deposit is set up in the system”

-

“Questions about payroll my school is sick with Covid”

-

“I have a question on a personal matter”

Payments and Charges Question:

-

“Billing not submitted to state title 20 assistance program & kindercare attempting to bill parent for kindercare being negligent with not billing state for payment.

” -

“Billing”

-

“Direct deposit”

”

”Product/ Service Question:

-

“Workmans comp department”

-

“Hey my Name DarleneDixon I used to work at kindercare .

I need to know when I was hied and the last day I work there.” -

“Insurance”

I need to know when I was hied and the last day I work there.”

I need to know when I was hied and the last day I work there.”Account Question:

-

“Having problelm login in adp”

-

“My login portal is not working”

-

“My account has been lock need to reset , because I don’t have my old cellphone number anymore”

Refund Question:

-

“Need refund”

-

“Refund”

Shipping and Delivery Question:

-

“Did not recieve a last paycheck”

Staff Question:

-

“Understaffed/ out of ratio”

Website/ Application Question:

-

“App”

Other Question:

-

“Bereavement Policy”

-

“I got a check in the mail from kindercare Education is this a real check”

-

“HR”

About

Edit Description

Compare KinderCare To

Companies are selected automatically by the algorithm. A company’s rating is calculated using a mathematical algorithm that evaluates the information in your profile. The algorithm parameters are: user’s rating, number of resolved issues, number of company’s responses etc. The algorithm is subject to change in future.

A company’s rating is calculated using a mathematical algorithm that evaluates the information in your profile. The algorithm parameters are: user’s rating, number of resolved issues, number of company’s responses etc. The algorithm is subject to change in future.

KinderCare

Overview

Reviews

Q&A

Contacts

KinderCare Learning Center Salaries | How Much Does KinderCare Learning Center Pay in the USA

- Home

- KinderCare Learning Center

- Employee Salaries

Filter by Job Title

Filter by Location

Nationwide

$38K

(119 salaries)

-$2K (5%) less than national average Teacher salary ($40K)

+$14K (45%) more than average KinderCare Learning Center salary ($24K)

$50K

$100K

$150K

+$6K (22%) more than average KinderCare Learning Center salary ($24K)

+$27K (72%) more than average KinderCare Learning Center salary ($24K)

-$4K (18%) less than average KinderCare Learning Center salary ($24K)

See 116 More KinderCare Learning Center Teacher Salaries

$38K

(1 salaries)

-$2K (5%) less than national average Coordinator salary ($40K)

+$14K (45%) more than average KinderCare Learning Center salary ($24K)

$50K

$100K

$150K

+$14K (45%) more than average KinderCare Learning Center salary ($24K)

“My salary compared to other bookkeeping/accounting positions is low. “

“

$25K

(46 salaries)

-$1K (3%) less than national average Lead Teacher salary ($26K)

+$1K (4%) more than average KinderCare Learning Center salary ($24K)

$50K

$100K

$150K

+$6K (22%) more than average KinderCare Learning Center salary ($24K)

+$4K (15%) more than average KinderCare Learning Center salary ($24K)

Equal to average KinderCare Learning Center salary ($24K)

See 43 More KinderCare Learning Center Lead Teacher Salaries

$28K

(40 salaries)

-$22K (56%) less than national average Assistant Director salary ($50K)

+$4K (15%) more than average KinderCare Learning Center salary ($24K)

$50K

$100K

$150K

+$11K (37%) more than average KinderCare Learning Center salary ($24K)

+$6K (22%) more than average KinderCare Learning Center salary ($24K)

+$1K (4%) more than average KinderCare Learning Center salary ($24K)

See 37 More KinderCare Learning Center Assistant Director Salaries

$27K

(30 salaries)

+$1K (3%) more than national average Preschool Teacher salary ($26K)

+$3K (11%) more than average KinderCare Learning Center salary ($24K)

$50K

$100K

$150K

+$17K (52%) more than average KinderCare Learning Center salary ($24K)

+$6K (22%) more than average KinderCare Learning Center salary ($24K)

+$6K (22%) more than average KinderCare Learning Center salary ($24K)

See 27 More KinderCare Learning Center Preschool Teacher Salaries

$47K

(21 salaries)

+$2K (4%) more than national average Center Director salary ($45K)

+$23K (64%) more than average KinderCare Learning Center salary ($24K)

$50K

$100K

$150K

+$17K (52%) more than average KinderCare Learning Center salary ($24K)

+$24K (66%) more than average KinderCare Learning Center salary ($24K)

+$10K (34%) more than average KinderCare Learning Center salary ($24K)

See 18 More KinderCare Learning Center Center Director Salaries

$30K

(21 salaries)

Equal to national average Teaching Assistant salary ($30K)

+$6K (22%) more than average KinderCare Learning Center salary ($24K)

$50K

$100K

$150K

+$6K (22%) more than average KinderCare Learning Center salary ($24K)

+$6K (22%) more than average KinderCare Learning Center salary ($24K)

-$6K (28%) less than average KinderCare Learning Center salary ($24K)

See 18 More KinderCare Learning Center Teaching Assistant Salaries

$22K

(18 salaries)

-$1K (4%) less than national average Toddler Teacher salary ($23K)

-$2K (8%) less than average KinderCare Learning Center salary ($24K)

$50K

$100K

$150K

Equal to average KinderCare Learning Center salary ($24K)

Equal to average KinderCare Learning Center salary ($24K)

-$4K (18%) less than average KinderCare Learning Center salary ($24K)

See 15 More KinderCare Learning Center Toddler Teacher Salaries

$35K

(13 salaries)

-$5K (13%) less than national average Program Specialist salary ($40K)

+$11K (37%) more than average KinderCare Learning Center salary ($24K)

$50K

$100K

$150K

+$6K (22%) more than average KinderCare Learning Center salary ($24K)

+$17K (52%) more than average KinderCare Learning Center salary ($24K)

+$6K (22%) more than average KinderCare Learning Center salary ($24K)

See 10 More KinderCare Learning Center Program Specialist Salaries

$28K

(13 salaries)

+$2K (7%) more than national average Teacher Assistant salary ($26K)

+$4K (15%) more than average KinderCare Learning Center salary ($24K)

$50K

$100K

$150K

-$4K (18%) less than average KinderCare Learning Center salary ($24K)

+$12K (40%) more than average KinderCare Learning Center salary ($24K)

+$6K (22%) more than average KinderCare Learning Center salary ($24K)

See 10 More KinderCare Learning Center Teacher Assistant Salaries

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- >

District Manager

is the highest paying job at KinderCare Learning Center at $77,000 annually.

Group Leader

is the lowest paying job at KinderCare Learning Center at $14,000 annually.

KinderCare Learning Center employees earn $24,000 annually on average, or $12 per hour.

- Smithtown, NY – 1

- Spring, TX – 1

- Suffern, NY – 1

-

1 salaries

-

1 salaries

-

1 salaries

-

1 salaries

-

1 salaries

-

1 salaries

-

1 salaries

-

1 salaries

-

1 salaries

-

1 salaries

- See more KinderCare Learning Center salaries by Location

Advertisement

-

Sila Inc.

– Portland, OR -

Braintrust – San Francisco, CA

-

Infinity Consulting Solutions – Brackettville, TX

-

Meta – Sunnyvale, CA

– Portland, OR

– Portland, ORInclusion Services Developer II – Remote Opportunity job at KinderCare Education in Portland, OR

Inclusion Services Developer II – Remote Opportunity

KinderCare Education

Full Time

Portland, OR

Posted Today

Apply This Job

Job description

About KinderCare Education®

KinderCare Education operates more than 1,380 early learning centers, and more than 560 Champions sites, supported by a corporate team of nearly 600 headquarters employees in Portland, Oregon. In 2019, KinderCare Education earned their third Gallup Great Workplace Award – one of only 39 companies worldwide to win this award.

- In neighborhoods with our KinderCare® Learning Centers that offer early childhood education and child care for children six weeks to 12 years old

- At work through KinderCare Education at Work™, family benefits for employers including on-site and near-site early learning centers and back-up care for last-minute child care

- In local schools with our Champions® before and after-school programs.

Job Summary:

The person filling this position will join the Education team in assisting Center Directors, other field leaders and teachers in creating inclusive environments for children of all abilities and backgrounds, supporting KinderCare Education’s mission of educating children throughout the United States. This position involves an interesting and unique combination of educational consulting, program material development, and legal compliance work, and is an outstanding opportunity for an early childhood education professional to make a meaningful difference for the children and families throughout the 2,000 + center and sites we operate in the United States.

Job Responsibilities:

This role is a part of the Education Programs team, responsible for developing tools that empower teachers to shape and change children’s lives, such as our curriculum, professional development experiences, and individualized consultation in best practices of inclusion. The Inclusion Services Advisor (ISA II) will be responsible for managing the Inclusion Services Hotline, which provides support to the field on a daily basis by responding to calls and emails regarding enrolling and retaining children of all abilities and backgrounds in our centers. Under the supervision of the Inclusion Services Manager, the ISA II will further develop, update, and deliver resources aimed at promoting inclusive practices in our centers, and works closely with the entire Education Programs team in the creative development, writing, and delivery of educational resources and trainings for KCE’s teachers across all brands.

Essential Functions:

- Generate innovative ideas, concepts, and solutions in response to field needs and requests related to supporting the inclusion and education of all children

- Advise field management on enrollment and retention issues for children and families with unique needs

- Develop, implement, and administer program material and processes related to differentiation in the early childhood classroom.

- Lead projects and initiatives at the direction of the Manager of Inclusion Services

- Develop and sometimes draft high-quality, culturally responsive educational resources and trainings according to project needs, timelines, and specifications

- Create, modify, and report on timelines and deliverables to Manager on a regular basis

- Represent KCE positively within ECE field and at professional gatherings, as needed

- Bachelor’s degree in Education or a related field strongly preferred; Master’s degree in Education, Special Education, or Teaching preferred

- 4 years of experience working with children in inclusive environments and direct childcare center or related experience strongly preferred

- At least 4 years of direct experience addressing behavior and mental health among elementary school-age children preferred

- Ability to use creative problem-solving skills to identify ways to meet children’s individual care needs and possible solutions to challenging behaviors

- Excellent interpersonal skills and ability to show empathy and to respond to the concerns of staff and parents in a caring manner with patience and active listening

- Ability to persuade outcomes in a collaborative manner, inspiring others to see challenging situations as opportunities for positive change

- Skilled at handling urgent situations with thoughtful analysis and judgment and calm temperament

- Excellent organizational skills, including consistent documentation of support provided to the field on specific issues

- Ability to work independently as well as collaborate with others

- Ability to meet deadlines, even under a heavy workload and to accept feedback and constructive evaluation of work

- Strong writing, presentation and verbal communication skills, including the ability to discuss technical information orally and in writing in easy-to-understand language

- A candidate with a strong combination of relevant work experience and education may be considered

Our highest priority has always been to keep our employees, children, families, and communities as safe and healthy as possible. Starting October 18, 2021, we began requiring COVID vaccinations or weekly COVID testing for all unvaccinated employees who are required to be in a KinderCare Education community space or workspace to perform their work (center, National Support Center, and offsite meeting environments). We are also subject to state law, local ordinances, and Health Department requirements for employees working in child care and school facilities.

Starting October 18, 2021, we began requiring COVID vaccinations or weekly COVID testing for all unvaccinated employees who are required to be in a KinderCare Education community space or workspace to perform their work (center, National Support Center, and offsite meeting environments). We are also subject to state law, local ordinances, and Health Department requirements for employees working in child care and school facilities.

KinderCare Education employs more than 32,000 team members across 1,700 locations nationwide. Our devoted family of education providers leads the nation in accreditation and includes KinderCare® Learning Centers, KinderCare Education at Work®, Champions® Before- and After-School Programs, Cambridge Schools™, Knowledge Beginnings® and The Grove School®.

KinderCare Education is an Equal Opportunity employer. All qualified applicants will receive consideration for employment without regard to race, national origin, age, sex, religion, disability, sexual orientation, marital status, military or veteran status, gender identity or expression, or any other basis protected by local, state, or federal law.

Primary Location : Portland, Oregon, United States

Job : Corporate

Save This Job

Apply Job

Related Jobs

All Related Listed jobs

[2022-23] High School Social Worker

Harlem Village Academies

New York, NY 10027

Today

The Opportunity Harlem Village Academies is a community of educators working to build an urban school district based on the ideals and tenets of progressive education. HVA is the lab school for

Caregiver – All Shifts

Visiting Angels

Owings Mills, MD 21117

Today

Get paid to interview – $20 CASH at new hire Orientation! Transportation Allowance – get paid to drive to work! PPE and Ongoing Training are provided to support your safety at work! Apply to

Banquet Server

Napa Valley Marriott

Napa, CA

Today

Why us? Sage Hospitality Group is set to hire a Banquet Server to join our award-winning team at the Napa Valley Marriott Hotel & Spa, home to modern and sophisticated charm and right amidst

Server

TG Administration LLC

Seaside, CA 93955

Today

Bayonet Black Horse Grill is hiring wait staff for this very busy summer season and beyond! We are looking for awesome, charming and hardworking personalities who have a strong passion

Supervisor, Meter Services

Bermex, Inc.

Today

We empower the best people to help sustain our world. 100% employee-owned. Independence guaranteed. Company: Bermex, Inc. Bermex is currently seeking energetic experienced professionals. Our

Administrative Specialist

RISE Services, Inc.

Salem, OR 97302

Today

This is a temporary position that is expected to last 6 months.This position is in-office; all COVID safety measures in place must be followed.The set pay rate for this position is $16.50 to

Clerical Professional

Eastchester Chrysler Jeep Dodge Ram

Bronx, NY 10466

30+ days ago

Seeking customer service oriented professionals for various roles throughout the dealership such as Greeters, Receptionists, Cashiers and File Clerks.

Director

Stanislaus Regional Transit Authority

Modesto, CA 95354

30+ days ago

Ensures the development and continuous improvement of transit. Agencies to coordinate regional issues and represent the Authority.

Login

User Name

Password

Remember Me

Lost Your Password?

Child Care job at KinderCare Learning Companies in Owings Mills, MD 21117

Apply This Job

Job description

Our mission will inspire you! Be a part of the Preschool Teacher team at city name KinderCare and share your compassionate spirit with us! We are looking to grow and develop our team with individuals who love educating young minds, all while creating lasting memories!

We are the ONLY national Child Care Provider to have earned the WELL Health/Safety Rating for our COMMITMENT to industry-leading health and safety standards!

We offer COMPETITIVE benefits and pay!

At KinderCare Learning Companies, we’re using our expertise in early childhood education to:

· Inspire lifelong learners by creating unique experiences for all children through our powerful curriculum

· Provide growth opportunities through enriching teacher development

· Live by core values that focus on strengthening relationships between everyone in our centers

We are committed to making our spaces inclusive for everyone – diversity and equality are essential to what we do. Help us develop warm and strong connections with each of our families and teachers to broaden our experiences and share different cultures!

Help us develop warm and strong connections with each of our families and teachers to broaden our experiences and share different cultures!

“It is our responsibility to challenge ourselves to do the work and nurture a diverse and inclusive environment, one where our employees and the children and families we serve are seen, heard, and valued.” – KLC Chairman and CEO Tom Wyatt

BENEFITS:

· Discounted childcare & perks

· Health and Wellness

· Financial and retirement

· Professional and Educational development

REQUIREMENTS:

- A commitment to nurturing and inspiring the children in your care

- A desire to partner with parents in their child’s education

- A willingness to create a positive team environment

- High school diploma minimum

- 90 clock hours (or course equivalent) in a specific age group – preferred

How will YOU inspire Brilliance in one of our classrooms? Take this opportunity to start or continue your career in Early Childhood Education! Apply today and recruiter name will reach out to you in the next few days to set up a phone interview!

Job Types: Full-time, Part-time

Schedule:

- 8 hour shift

- Monday to Friday

Application Question(s):

- Tell me more about your childcare experience.

Education:

- High school or equivalent (Required)

Work Location: One location

Save This Job

Apply Job

Related Jobs

All Related Listed jobs

CNAI – ACUTE

UNC Health Blue Ridge

Today

JOB SUMMARY: Assists the nurse in planning/implementing basic care as delegated. Demonstrates knowledge/skills necessary to provide care appropriate to the age and culture of the residents/patients

Customer Service – Work From Home

Staffmark

Grapevine, TX 76051

Today

Do you love helping and providing quality customer service? This could be the perfect fit for you! Virtual Call Center Representative needed for a temp to hire opportunity!! MUST HAVE 6 MONTHS

Benefit Analyst

ZimVie

Westminster, CO

23 days ago

We currently have an opportunity for a Benefits Analyst that offers exposure to a wide range of programs in a fast-paced environment.

Server

Hillstone Restaurant Group

Denver, CO 80206

Today

Hillstone in Denver currently seeking exceptional candidates to join our service team. We are searching for friendly, energetic, highly motivated individuals who will thrive in a fast-paced,

Pet Retail Team Member

My Pet Market

Today

My Pet Market Overview: We are a multi-store company that is truly dedicated to our customers and their animals by helping them find the best natural and holistic products for their pet. We pride

Dental Office Front Desk Administrator

Orthodent Management LLC

Luling, TX 78648

Today

An upbeat general dental office in Luling is looking for a front desk administrator. Experience preferred but will train the right candidate. A full job description is as follows:

Experience preferred but will train the right candidate. A full job description is as follows:

Login

User Name

Password

Remember Me

Lost Your Password?

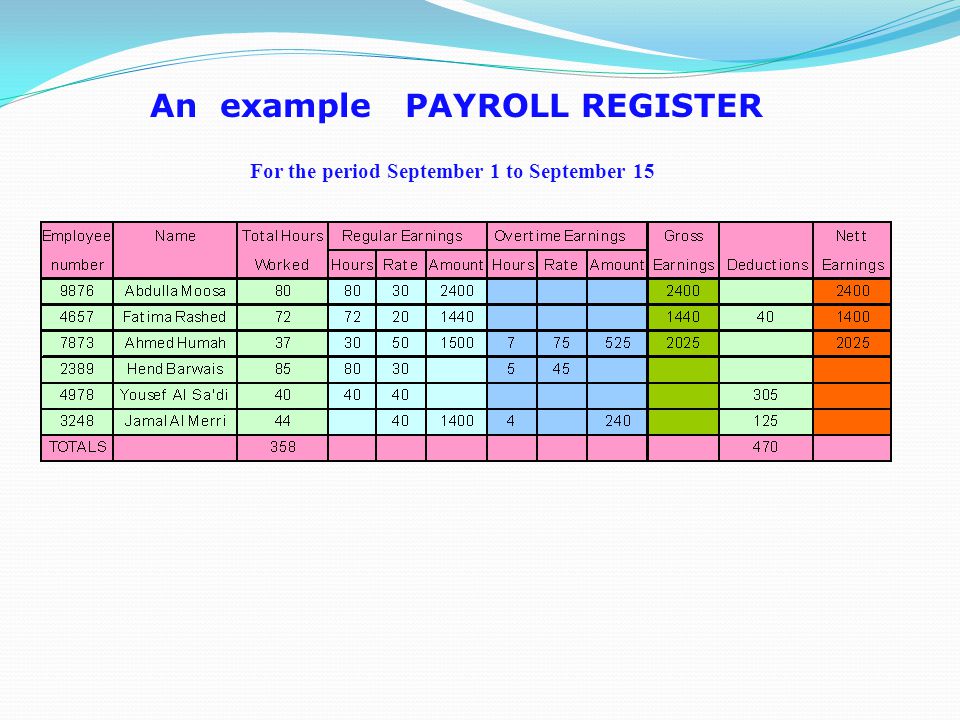

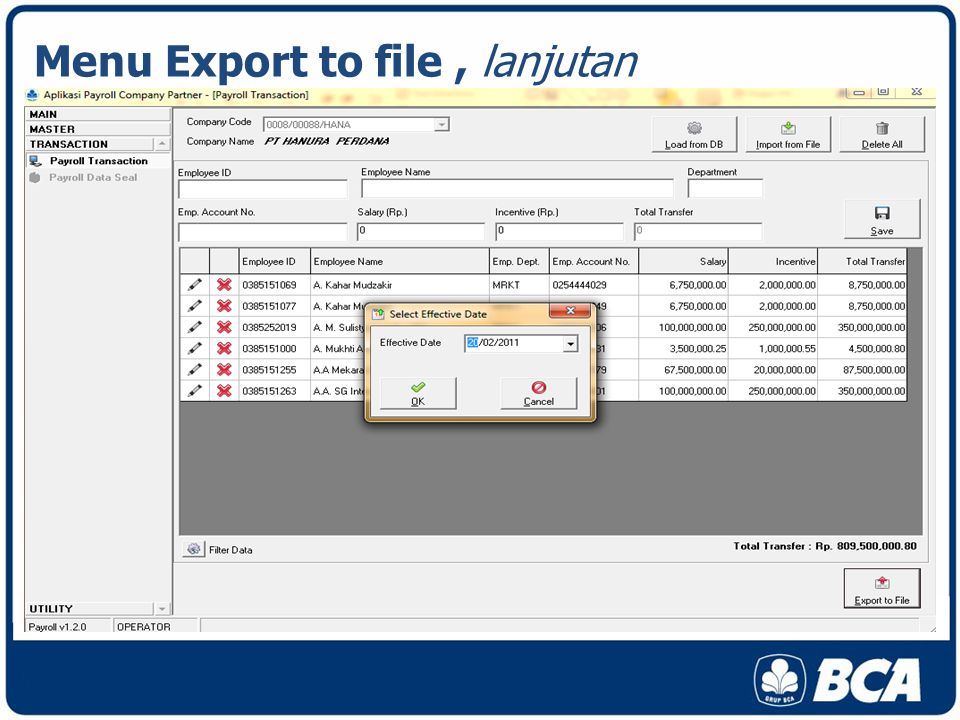

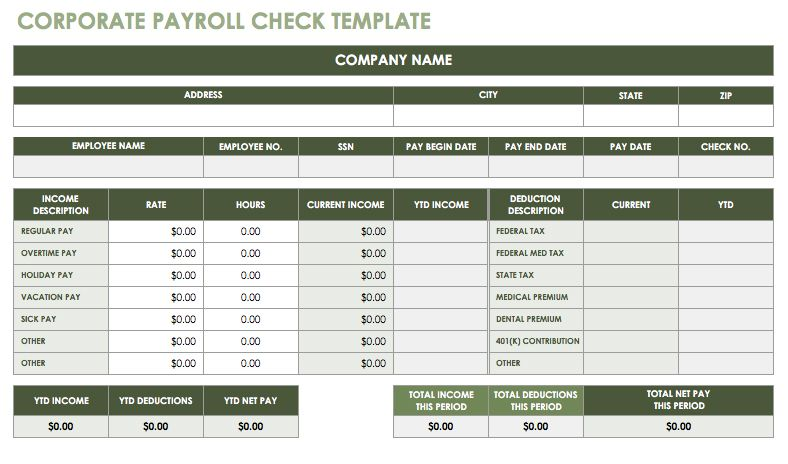

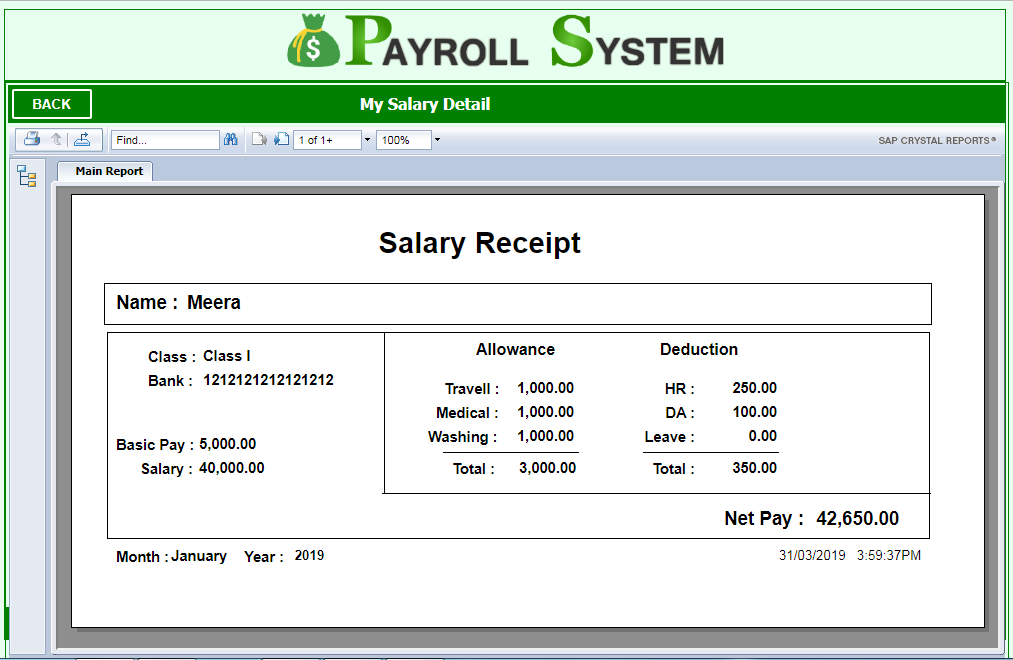

Payroll for the issuance of wages in the form No. T-53

Payroll for the issuance of wages – you can download it on our website – an important accounting document used within the company. Our material will help to study the procedure for filling it out and learn about the requirements.

Unified form or arbitrary

Payroll is one of the accounting documents used within the company that confirm the procedure associated with the issuance of cash from the cash desk.

Given the right of companies to independently develop primary accounting documents, the question arises: is it possible to invent, approve and apply the payroll on our own, or will we have to be content with the unified T-53 form that is familiar to everyone?

The answer to this question is contained in the information of the Ministry of Finance dated 04. 12.2012 No. ПЗ-10/2012, from which it is clear that since 2013 it is not necessary to apply unified forms of documents.

12.2012 No. ПЗ-10/2012, from which it is clear that since 2013 it is not necessary to apply unified forms of documents.

However, this does not apply to all primary organizations – the forms established by the authorized bodies on the basis of federal laws remained mandatory. Payroll can be classified as such papers.

IMPORTANT! The use of the payroll is regulated by the Instruction of the Central Bank dated March 11, 2014 No. 3210-U on the conduct of cash transactions.

In order not to violate the procedure for conducting cash transactions, you should use payroll 0301011 (paragraph 2, clause 6 of Instruction No. 3210-U). Payroll index corresponding to OKUD 0301011: T-53. This form is approved as unified by the Decree of the State Statistics Committee of Russia dated 01/05/2004 No. 1.

You can find a step-by-step algorithm for issuing salaries from the cash desk in ConsultantPlus. Get a trial access to the system for free and go to the Ready solution.

You can download the payroll form in the T-53 form on our website:

Download the T-53 form

funds to the person entitled to it. Registration of this procedure can be carried out with the help of other documents – they are provided for by the same Instruction No. 3210-U.

For example, you can pay a salary to one person using an account cash warrant (form No. KO-2), and arrange a group payment using a payroll statement (form T-49).

The materials of our website will help to document the issuance of wages:

- “Unified form No. T-49 – form and sample” ;

- “Unified Form No. KO-2 – Cash Debit Order” .

Mandatory sections of the payroll sheet

The payroll form begins with the name of the company and its structural unit.

Separately, in the T-53 form, a field is filled in to reflect the corresponding account – when paying salaries, account 70 “Settlements with personnel for wages” is indicated.

Then the information is entered into the cells according to the timing of the payment of money. Then the total amount issued according to the statement is filled in (in numbers and in words).

IMPORTANT! The duration of the time period during which it is permissible to issue salaries from the cash desk and make other payments is established by paragraph 6.5 of Directive No. 3210-U and is 5 working days (including the day the cash is received from the bank).

This information is followed by the signatures of the responsible persons of the company: the head and the chief accountant.

You must also indicate the number of the payroll and the date it was compiled.

Payrolls for the issuance of wages (a form for which you can download on our website) contain one more additional field – to reflect the billing period. This information is important for the correct registration of the payroll transaction in accounting registers.

In addition to the signatures of the director and the chief accountant, the payroll contains the signatures of several more responsible persons: the accountant who checked the execution of payments; the specialist who carried out the payroll operation (cashier or other authorized person). The indicated signatures with full name decoding complete the payroll.

The indicated signatures with full name decoding complete the payroll.

We will tell you about filling in the tabular part of the payroll in the next section.

Important! Hint from ConsultantPlus

You can correct your payroll if you find an error. It can be fixed…

See K+ for more details, having received a free trial access.

Accruals payable: filling out the tabular part of the statement

Filling in the tabular part of the T-53 form is based on the payroll sheet. Accruals are made by the company’s specialists on the basis of salaries, tariffs, piece rates – depending on the forms of remuneration used in the company.

Before entering information about earned funds in the tabular part of the payroll, the necessary deductions (alimony, compensation for damage, etc.) are made from the accrued amounts, personal income tax is deducted. The result of the calculations is entered in column 4 of the payroll.

Each amount of the calculated salary is entered in a separate line of the tabular part of the payroll sheet (you can download the form on our website).

To personify the accrued amounts in the statement, columns 2–3 are intended, which contain information about the payroll number and full name of the recipient.

Column 5 of the payroll table is intended to confirm the fact that funds have been issued from the cash desk or to mark the deposit of unpaid amounts. Note that from November 30, 2020, the requirement to put a note on the payroll about the deposit of wages not received by employees has been canceled.

Column 6 “Note” deserves special attention. In a normal situation, when employees of the company personally receive money, it is not filled out. Information appears in it, for example, when issuing salaries by proxy. In this case, in the indicated line, the cashier makes an entry “by proxy”, and the power of attorney itself is attached to the payroll (clause 6.1 of Directive No. 3210-U).

Where to see a sample payroll

You can download a sample payroll from our website:

Download a sample payroll

Summary

Payrolls include many mandatory fields: payments of funds up to a detailed indication of the amounts of salaries paid.

Such a statement is signed by several people: the head of the company, the responsible person who made the payment, the chief accountant and the accountant who performs control functions.

$92,736,310

$0

$0 (-$10,236,310 )

$89,695,833

$0

$0 (-$7,195,833 )

$ 89,695,833

$ 0

$ 0 (-$ 7,195,833)

11.09.22

9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000

$89,281,333

$0

$0 (-$6,781,333 )

$89,281,333

$0

$0 (-$6,781,333 )

09.22

09.22 $88,821,666

$ 0

$ 0 (-$ 6,321,666)

$ 88,821,666

$ 0

$ 0 (-$ 6,321,666)

9 110119

$85,875,834

$0

$0 (-$3,375,834 )

$85,875,834

$0

$0 (-$3,375,834 )

$ 85,251,667

$ 0

$ 0 (-$ 2.751.667)

$0 (-$2,751,667 )

$85,116,917

$0

$0 (-$2,616,917 )

$85,116,917

$0

$0 (-$2,616,917 )

09.22

09.22 $84,873,107

$0

$0 (-$2,373,107 )

$84,873,107

$0

$0 (-$2,373,107 )

$84,741,667

$0

$0 (-$2,241,667 )

$ 84.741.667

$ 0

$ 0 (-$ 2,241,667)

11.09.22

2

6 ToronTO Toronto Toronon LEAPLE TORPLE0116

$83,993,116

$0

$0 (-$1,493,116 )

$83,993,116

$0

$0 (-$1,493,116 )

$83,980,175

$ 0

$ 0 (-$ 1,480,175)

$ 83,980,175

$ 0

$ 0 ($ 1.

480.175)

480.175)

9 9019 2

$82,426,625

$0

$73,375

$82,426,625

$0

$73,375

$82,270,001

$0

$229.999

$82,270,001

$0

4 $22

$82,083,333

$0

$416,667

$82,083,333

$0

$416,667

$81,875,000

$0

$625,000

$81,875,000

$0

$625,000

$81,491,469

$0

$1,008,531

$81,491,469

$0

$1,008,531

09.22

09.22 $81,489,166

$0

$1,010,834

$81,123,334

$0

$1,376,666

$81,123,334

$0

$1,376,666

$2,136,667

$80,363,333

$0

$2,136,667

$80,139,963

$0

$2,360,037

$80,139,963

$0

$2,360,037

$80,105,309

$0

$2,394,691

$80,105,309

$0

$2,394,691

09.22

09.22 $78,590,000

$0

$3,910,000

$78,590,000

$0

$3,910,000

$76,970,357

$0

$5,529,643

$76,970,357

$0

$5,529,643

$76,761,921

$0

$5,738,079

$76,761,921

$0

$5,738,079

$76,164,166

$0

$6,335,834

$76,164,166

$0

$6,335,834

$75,459,881

$0

$7,040.

119

119

$75,459,881

$0

$74,959,296

$0

$7,540,704

$74,959,296

$0

$7,540,704

$74.328.889

$0.

$0

$8,171,111

$65,901,667

$0

$16,598,333

$65,901,667

$0

$16,598,333

$62,895,834

$0

$19.6060124

$62,895,834

$0

$19,604,166

09.22

09.22 $62,136,709

$0

$20,363,291

$62,136,709

$0

$20,363,291

Unified form N T-49.

Payroll • Handbook of legislation “Science, legislation and law”

Science, education and law

Payroll

Unified form N T-49

Approved by resolution

State Statistics Committee of the Russian Federation

dated January 5, 2004 N 1

(see Instructions for use and

filling out forms of primary accounting documentation)

------------+

¦ Code ¦

+-----------+

Form according to OKUD¦ 0301009¦

+-----------+

according to OKPO¦¦

-------------------------------------------------- - +-----------+

name of the organization

¦ ¦

-------------------------------------------------- -+--------------------

structural subdivision

To the cashier for payment on time from " "____________ 20 to "" ____________ 20

Sum _________________________________________________________________________

in words

________________________________ rub _______ kop (__________ rub ____kop)

figures

Head of the organization _________ ______________ ______________________

position personal signature signature transcript

Chief Accountant ______________ ___________________

personal signature signature transcript

------------T-------------+ ------------------+

¦ Number ¦ Date ¦ ¦ Reporting period ¦

¦ document ¦ drafting ¦ ¦ ¦

+-----------+-------------+ +--------T--------+

¦ ¦ ¦ ¦ from ¦ to ¦

L-----------+-------------- +--------+--------+

"" ___________ 20. Payroll ¦ ¦ ¦

L--------+---------

--------T--------T---------T------------T--------- ---------------T---------------------------------- ---------+

¦ Number ¦ Timesheet- ¦ Position ¦ Tariff ¦ Days worked (hours) ¦ Accrued, rub ¦

¦ to ¦ ny ¦ (special ¦ rate ¦ +-----------------------------------T-- -----+

¦order¦ number ¦fullness, ¦ (hourly, ¦ ¦ for the current month (by type of payment) ¦ total ¦

¦ ¦ ¦profession¦ daytime) +------T--------T--------+---T---T----T---- T---T-------------+ ¦

¦ ¦ ¦) ¦ (salary), rub ¦ work- ¦ weekends ¦ holidays-¦ ¦ ¦ ¦ ¦ ¦ other income¦ ¦

¦ ¦ ¦ ¦ ¦ sneeze ¦ ¦ full ¦ ¦ ¦ ¦ ¦ ¦ in the form of ¦ ¦

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ various ¦ ¦

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ social and ¦ ¦

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ material ¦ ¦

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ good ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ 1 ¦ 2 ¦ 3 ¦ 4 ¦ 5 ¦ 6 ¦ 7 ¦ 8 ¦ 9¦ 10 ¦ 11 ¦12 ¦ 13 ¦ 14 ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+-------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

L-------+--------+---------+------------+------+-- ------+--------+---+---+----+----+---+------------ -+--------

-----------------T---------------------- ----T--------------------------+

¦ Withheld and set off, rub ¦ Amount, rub ¦ Received money ¦

+-----------T----T---T----+-----------------T---- ----+-------------T------------+

¦ tax on ¦ ¦ ¦ ¦ debt ¦ to ¦ surname, ¦ signature ¦

¦ income ¦ ¦ ¦ +---------T--------+ payment ¦ initials ¦ (record about ¦

¦ ¦ ¦ ¦ ¦ for ¦ for ¦ ¦ ¦deposit- ¦

¦ ¦ ¦ ¦ ¦ organization-¦employee-¦ ¦ ¦ nii sum) ¦

¦ ¦ ¦ ¦ ¦ sion ¦ com ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ 15 ¦ 16 ¦17 ¦ 18 ¦ 19¦ 20 ¦ 21 ¦ 22 ¦ 23 ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+-----------+----+---+----+---------+--------+---- ----+-------------+------------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

L-----------+----+---+----+---------+--------+---- ----+-------------+-------------

2nd page of form N T-49---------T----------T----------T----------T------- ---------------T---------------------------------- --------+

¦Personnel number ¦Position ¦Tariff ¦Worked out ¦Acrued, rub ¦

¦order ¦ number ¦(special-¦ rate +----------------------+---------------- -------------------T------+

¦ ¦ ¦ availability, ¦ (hourly, ¦ days (hours) ¦ for the current month (by type of payment) ¦ total ¦

¦ ¦ ¦ profession) ¦ daytime), ¦ ¦ ¦ ¦

¦ ¦ ¦ ¦ salary, rub ¦ ¦ ¦ ¦

¦ ¦ ¦ ¦ +------T-------T-------+---T---T---T----T----- T------------+ ¦

¦ ¦ ¦ ¦ ¦work- ¦exit- ¦holiday- ¦ ¦ ¦ ¦ ¦ ¦ other ¦ ¦

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ personal ¦ ¦ ¦ ¦ ¦ ¦ income in ¦ ¦

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ form ¦ ¦

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ various ¦ ¦

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦social and¦ ¦

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦material¦ ¦

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ good ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ 1 ¦ 2 ¦ 3 ¦ 4 ¦ 5 ¦ 6 ¦ 7 ¦ 8 ¦ 9¦10 ¦ 11 ¦ 12 ¦ 13 ¦ 14 ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

L--------+----------+----------+----------+------+ -------+-------+---+---+---+----+-----+----------- -+-------

-----------------------T-----------------------T-- ----------------------+

¦ Withheld and credited, ¦ Amount, rub ¦ Money received ¦

¦ rub ¦ ¦ ¦

+----------T---T---T---+----------------T------+-- ------------T---------+

¦ tax on ¦ ¦ ¦ ¦ debt ¦ to ¦ surname, ¦ signature ¦

¦ income ¦ ¦ ¦ +--------T-------+ pay-¦ initials ¦ (record o¦

¦ ¦ ¦ ¦ ¦ for ¦ for ¦ those ¦ ¦deposit-¦

¦ ¦ ¦ ¦ ¦ organization- ¦ work- ¦ ¦ ¦ ¦

¦ ¦ ¦ ¦ ¦ name ¦ nickname ¦ ¦ ¦ amount) ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ 15 ¦16 ¦17 ¦18 ¦ 19¦ 20 ¦ 21 ¦ 22 ¦ 23 ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦

+----------+---+---+---+--------+-------+------+-- ------------+---------+

¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦