Care com taxes: How to pay nanny taxes yourself

How to pay nanny taxes yourself

What can we help you find?

ArrowLeftRed

SearchRed

SearchClose

Back

4 steps to managing taxes and payroll for your household employee

If you pay your nanny or child care provider at least $2,600 in the 2023 calendar year, the IRS expects you to pay what’s known as the “nanny tax.” This year-round process is completed in four basic steps, and while many families choose to have HomePay do everything for them, it’s possible to do these items yourself.

- Complete the required setup paperwork

- Calculate payroll each pay period

- Send taxes to the IRS and state throughout the year

- Prepare year-end tax documents

Before you dive in, it’s a good idea to understand all these steps, so here’s a general idea of what you can expect to do if you choose to pay nanny taxes yourself:

1. Complete some initial paperwork

You can’t begin calculating payroll for your nanny without knowing how much in taxes to withhold. To do this, you’ll need your nanny to fill out Form W-4 and a state withholding form (if your state collects income taxes).

Because you are, technically, the employer of your nanny, you’ll also need to apply for a Federal Employer Identification Number (FEIN) with the IRS, as well as state tax identification numbers with the agencies that handle collection of state taxes. These tax IDs identify you as a household employer and are required for sending in tax returns. You should apply for you tax IDs once you’ve made the decision to hire a nanny.

2. Accurately calculate payroll each pay period

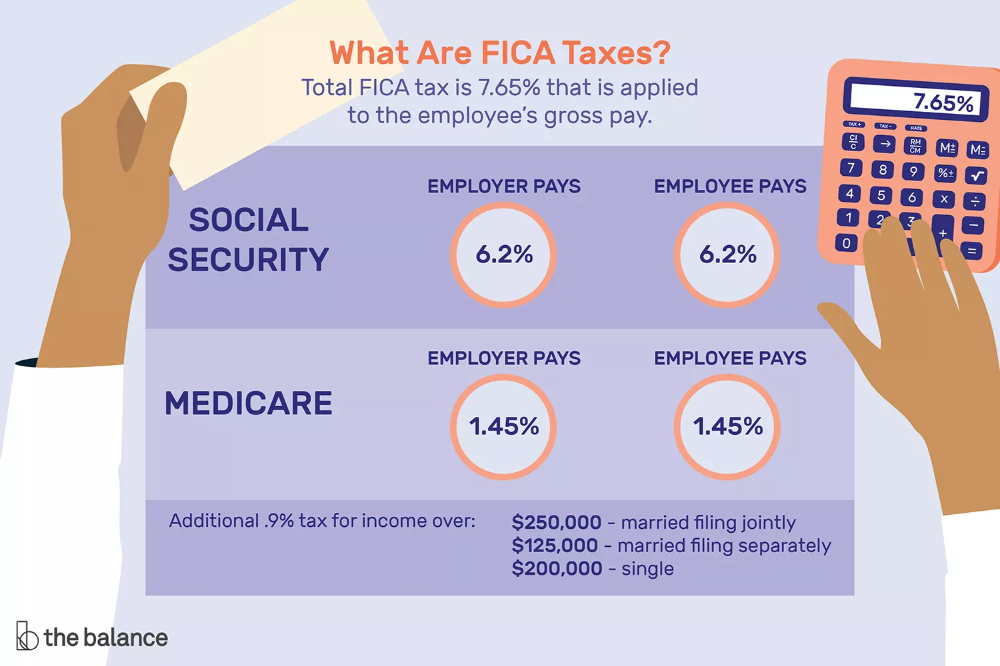

You’ll need to keep track of the hours your nanny works, apply their hourly rate and add any overtime pay to get to the gross (before taxes) amount. From there, you’ll need to withhold the correct amount of Social Security & Medicare taxes, income taxes, and any other state or local taxes that may apply. After these deductions, you’ll know how much your nanny’s net, or take-home, pay will be.

After these deductions, you’ll know how much your nanny’s net, or take-home, pay will be.

See how much a nanny costs where you live.

You’ll also need to calculate how much in Social Security & Medicare taxes, unemployment insurance taxes and any other miscellaneous state taxes you have accumulated as a household employer. These household employment taxes will generally be about 10% of the gross wages paid to your nanny, but can vary depending on where you live.

3. Send tax payments and returns to the IRS and the state

Your state requires you to send in tax returns—generally on a quarterly basis—for unemployment insurance taxes and income taxes. You’ll need to keep track of when these returns are due and send the appropriate amount of taxes to the correct agency. Some states have a different filing schedule so check your state’s requirements for more details.

Additionally, it’s recommended to send in estimated tax payments to the IRS four times per year to account for the Social Security & Medicare taxes you’re withholding from your nanny and accumulating for yourself. Waiting until you file your personal income tax return in April can result in underpayment penalties.

Waiting until you file your personal income tax return in April can result in underpayment penalties.

4. Prepare your year-end tax documents

After the year ends, you’ll need to prepare several documents to wrap up your annual nanny tax requirements:

-

Form W-2 for your nanny, so they can file their personal income tax return.

-

W-2 Copy A and Form W-3 to be filed with the Social Security Administration.

-

A state Annual Reconciliation Form if your state requires it.

-

Schedule H for you to attach to your personal income tax return.

The IRS estimates this work will take the average family 50-55 hours per year to administer. If you’d like to have those hours back in your life and enjoy the peace of mind of having an expert handle it all for you, give HomePay a call. We’ve helped families with these requirements since 1992 and can make the process a breeze.

Next Steps:

-

Find out how much to pay a nanny in your area

-

Use our nanny tax calculator to estimate your tax costs

-

See a demo of the HomePay nanny tax service

Get started with HomePay!

Already enrolled with HomePay? Log in

Like what you’re reading?

Join Care for FREE

Email is required.

Click ‘Next’ to start an account and get tips, tricks and trending stories.

Already Registered

The email address you entered is already registered. Would you like to log in?

Log in

Almost done!

Join Care for FREE

Create a free account to access our nation wide network of background checked caregivers.

First name

First name is required.

Last name

Last name is required.

Zip code

Zip code is required.

We’re sorry, your request could not be processed at this time. Please click here to try again.

By clicking “Join now,” you agree to our Terms of Use and Privacy Policy.

Welcome to Care!

You’re on your way to finding someone your family will love.

Start now

Tax breaks and credits for families hiring a nanny

What can we help you find?

ArrowLeftRed

SearchRed

SearchClose

Back

Learn how much money you can save by paying your nanny legally

One of the most common concerns families have when they hire a nanny is how much in taxes they’ll be responsible for paying. The good news is that families can qualify for at least one – if not two – tax breaks that can make paying their nanny on the books less expensive than paying under the table.

What tax breaks are available when I pay my nanny legally?

1. Dependent Care Account. A type of Flexible Spending Account (FSA), this tax break is available through the benefits package offered by most companies. You can use an FSA to pay for up to $5,000 of child care-related expenses – such as your nanny’s pay – using pre-tax dollars. Depending on your marginal tax rate, using an FSA can save around $2,000 in 2023. For enrollment details, check with your HR or Accounting Department.

2. Child or Dependent Care Tax Credit. To take this tax break, use IRS Form 2441 to itemize care-related expenses on your federal income tax return. A majority of families will receive a 20% tax credit on up to $3,000 of care-related expenses if you have one child, or $6,000 of care-related expenses if you have two or more children. This means your tax credit is up to $600 for one child and $1,200 for two or more children.

This means your tax credit is up to $600 for one child and $1,200 for two or more children.

How can I maximize my savings using child care tax breaks?

If you have one child, your best option is the FSA. Setting aside the full $5,000 will save about $2,000, depending on your marginal tax rate. If you don’t have access to an FSA (or cannot enroll at the moment), use the Child or Dependent Care Tax Credit.

If you have two or more children, you may be able to take advantage of both tax breaks. Use your FSA for the full $5,000 and if you have leftover child care expenses, you can apply another $1,000 toward the Child or Dependent Care Tax Credit. This combination saves you an additional $200 per year, which brings your total savings to about $2,200 for 2023.

How do I qualify for a nanny tax deduction?

“The most important thing to remember is that you can’t qualify for a tax break on your child care expenses if you aren’t paying your nanny legally,” says Tom Breedlove, Sr. Director of Care.com HomePay.

Director of Care.com HomePay.

Assuming this is not an issue, these tax breaks are available to you if your children are under the age of 13 and you have care-related expenses because both you and your spouse work, are looking for work or are full-time students. Child care expenses can be your nanny’s wages, the wages paid to a backup child care provider, the taxes your incur on your nanny’s wages and even the money paid to a placement agency.

When you sign up for Care.com HomePay, the paystubs we generate for you can serve as proof of child care expenses. This will allow you to use your FSA and/or keep track of how much to apply to the child care tax credit.

Next Steps:

-

Use our budgeting calculator to see your tax costs and tax breaks

-

Learn about the tax and payroll responsibilities you have when hiring a nanny

-

Find the right nanny to care for your kids

* The information contained in this article is general in nature, may not be applicable to your specific circumstances, and is not intended to be a substitute for or relied upon as personalized tax or legal advice.

Get started with HomePay!

Already enrolled with HomePay? Log in

Like what you’re reading?

Join Care for FREE

Email is required.

Click ‘Next’ to start an account and get tips, tricks and trending stories.

Already Registered

The email address you entered is already registered. Would you like to log in?

Log in

Almost done!

Join Care for FREE

Create a free account to access our nation wide network of background checked caregivers.

First name

First name is required.

Last name

Last name is required.

Zip code

Zip code is required.

We’re sorry, your request could not be processed at this time. Please click here to try again.

By clicking “Join now,” you agree to our Terms of Use and Privacy Policy.

Welcome to Care!

You’re on your way to finding someone your family will love.

Start now

90,000 individual entrepreneurs without income: how much to pay taxes?

It often happens that a person registers an individual entrepreneur, but the business never starts. The main thing you need to know is that even a non-working entrepreneur accumulates debt on annual insurance premiums. Other debts on an inactive individual entrepreneur are not always there. But we will be paranoid and tell you how to check all possible ones.

To stop the accumulation of debt, it is necessary to close the IP. Since the end of 2020, the tax office has been doing it itself. But with this outcome, a person will be banned from being an entrepreneur for three years.

Now about everything in order.

A non-working individual entrepreneur always accumulates a debt on insurance premiums

An individual entrepreneur without employees pays insurance premiums for himself to receive an old-age pension and medical assistance under the policy. Contributions go to the Social Fund of Russia. But they pay them in one window – to the tax office.

Contributions go to the Social Fund of Russia. But they pay them in one window – to the tax office.

The amount of contributions for individual entrepreneurs without employees consists of two parts. Fixed – its state establishes for each year. And additional – it is paid in the amount of 1% of income exceeding 300,000 rubles. A non-working individual entrepreneur has exactly a fixed part of the contributions for each year. But the tax authority can collect debt only for the last three years – this is a restriction from Art. 113 of the Tax Code of the Russian Federation.

The fixed part of contributions for 2023 is 45,842 rubles. You can see the contributions for previous years here. You can calculate the amount for all the years of the existence of an individual entrepreneur in the calculator on the tax website. If the IP was not opened at the beginning of the year, the amount of contributions is reduced in proportion to calendar days. If it is closed before the end of the year – the same. This follows from Art. 430 of the Tax Code of the Russian Federation.

This follows from Art. 430 of the Tax Code of the Russian Federation.

The due dates for payment of fees are as follows. The fixed part is paid every year until December 31st. Additional part – until July 1 of the next year. When an individual entrepreneur is closed, debts are paid within 15 days after deregistration with the tax office. It says so in Art. 432 of the Tax Code of the Russian Federation.

For violation of the deadlines for paying contributions, the tax authority charges penalties. The size is 1/300 of the key rate. But more than the body of the debt, penalties cannot be calculated – Art. 75 of the Tax Code of the Russian Federation.

Penalty calculator

If an individual entrepreneur did not sell anything, did not open an account and did not hire employees, he still pays insurance premiums. Entrepreneurs asked if it was legal in the Constitutional Court. They said so. A person opens an IP voluntarily. This means that he has the necessary money, education and skills to work and fulfill tax obligations – Definition No. 164-O.

164-O.

However, there are still periods for which insurance premiums may not be paid. They are spelled out in paragraph 7 of Art. 430 of the Tax Code of the Russian Federation:

– service in the army;

– care for a child up to 1.5 years old, but not more than 6 years old for all children;

– caring for a disabled person of group I, a disabled child or an elderly person over 80 years old;

– the period of residence with a spouse in a military unit or abroad in a diplomatic mission. but within 5 years.

In order for the tax authorities to cancel the contributions, you must bring documents that confirm these circumstances. Automatic accrual will not be canceled.

Other life circumstances are unlikely to get rid of the debt. For example, the court refused to cancel contributions to an entrepreneur who had been in prison for 6 years and did not work. The refusal was explained by the fact that even from places of deprivation of liberty it is possible to close an individual entrepreneur through a representative, and not accumulate debt – case No. A34-10340/2019.

A34-10340/2019.

If there was no income, it is necessary to submit a zero declaration

Usually, when registering, an entrepreneur chooses a special taxation regime – the simplified tax system or a patent. They do this because special regimes pay less taxes. But if the application does not reach the hands, the individual entrepreneur remains on the general taxation system and pays personal income tax, VAT and property tax.

The only way to find out your tax regime is to call or go to the tax office.

Entrepreneurs on the simplified tax system and the general system once a year or quarter submit a declaration to the tax office, even if they did not earn. So before the inspectors they confirm that there was no income and no tax should be paid. A declaration without income is called zero. For each failure to file a tax return, the tax authority fines 1,000 rubles under Art. 119 of the Tax Code of the Russian Federation. But you can fine only for the last three years.

The penalty for non-delivered zero declarations is added to the debt for unpaid insurance premiums and penalties to them.

🧮 It turns out that the tax debt of a non-working individual entrepreneur is the sum of insurance premiums for the last three years + penalties for late payment + fines for declarations.

How to find out about all the debts of an individual entrepreneur to the tax office

You can find out the full and exact amount of the debt through Internet services or by going personally to the tax office at the place of residence.

You can see the address of your tax office and make an appointment here. At the reception, it is worth asking the inspector for a Statement of the status of settlements and an extract of operations on settlements with the budget. These documents show the total amount of the debt and due to what payments and fines it appeared.

You can find out about debts without leaving your home and immediately pay them off on the Internet:

– In the Tax Debt section through your personal account on Public Services;

– In the personal account of the individual entrepreneur on the website of the Federal Tax Service. You can enter the account through an account from the State Services or using an EDS, if any.

You can enter the account through an account from the State Services or using an EDS, if any.

Tax debts do not just hang out in the personal account of an individual entrepreneur. First, the tax office sends a demand for payment, and then tries to write off money from all known accounts and personal cards of the entrepreneur. Inspectors can do this – art. 76 of the Tax Code of the Russian Federation.

If the inspectors do not find money in the accounts, the debt is transferred to the bailiffs. They can come home and take the property. You can find your business in the data bank of enforcement proceedings.

New IP – the year of the Elbe as a gift

Year of online accounting at the Premium rate for sole proprietors under 3 months

Try for free

Litigation involving individual entrepreneurs

Sometimes the situation with a business develops like this. They opened an individual entrepreneur, did a little work, but the business didn’t work, and everyone was abandoned.

They opened an individual entrepreneur, did a little work, but the business didn’t work, and everyone was abandoned.

Even if an entrepreneur did not sell goods or rent premises for a very short time, he could still have debts to clients and contractors. The pre-trial claims they sent in the mail are easy to miss. And perhaps the entrepreneur has already been sued.

You can find out about court cases with suppliers, contractors and landlords in the file of arbitration cases. This is the basis of all litigation between entrepreneurs.

If there is a danger that claims from individual clients remain against individual entrepreneurs, it is worth checking the database of courts of general jurisdiction in the GAS Justice service.

If you find out that you are a participant in a court case, you should immediately connect. Go to court, photograph the statement of claim and evidence in the materials. Then go to court sessions, argue or try to go to the world.

How to deal with an unnecessary IP

An idle IP should be closed. This will stop the accumulation of debts on contributions. But the debts themselves are not going anywhere. Debts will remain hanging on individuals, and sooner or later they will have to be paid off.

This will stop the accumulation of debts on contributions. But the debts themselves are not going anywhere. Debts will remain hanging on individuals, and sooner or later they will have to be paid off.

If you close the IP on your own, in the future it will be possible to open a new one. Closing an IP without employees is simple, fast and almost free. Check out our article on this.

It is impossible to sell or re-register an individual entrepreneur to another person.

Non-working individual entrepreneurs are closed by the tax authorities themselves, but this is not always good

From the end of 2020, the tax authorities will close non-performing individual entrepreneurs Speaking in legal terms, it excludes an entrepreneur from the unified state register under Art. 22.4 of Law No. 129-FZ.

Individual entrepreneurs are considered non-working if two conditions are met:

– they have not submitted calculations and declarations for more than 15 months or have not renewed the patent,

– there is an outstanding debt for taxes or contributions.

Before exclusion, the tax office is trying to find creditors for individual entrepreneurs. To do this, a message is published in the journal “Bulletin of State Registration” about the upcoming closure of the IP. If within a month none of the suppliers, customers or former employees make their claims, the IP will be liquidated.

Exclusion from the unified state register stops the accumulation of debts. But, as in the case of voluntary closure, all accrued taxes and contributions are transferred to an individual.

Leaving an individual entrepreneur and waiting for the tax authorities to deal with it is not beneficial for everyone and not always. Over the next three years, a person whose IP was closed by the tax office will not be able to open a new one. And also – it is not known when the inspectors will get specifically to your individual entrepreneur. And all this time, the amount of debt will grow like a snowball.

The article is relevant to

Russians will be “additionally charged” for tax evasion

Fresh number

RG-News

Rodina

thematic applications

Union

Fresh number

06. 04.2021 12:37

04.2021 12:37

Category:

Voronezh

Dmitry Efremov (lawyer-lawyer Tax-analyst Tax Compleans )

The Federal Tax Service of Russia has revised its approach to additional charges due to tax evasion. Each paragraph of the letter on the practice of applying Article 54.1 of the Tax Code summarizes the practice of arbitration courts in resolving disputes on the most pressing tax risks.

The letter reflects positions and approaches that have either been developed by the highest courts or have been tested by thousands of tax disputes. Along with clarifications on the criteria and methods for analyzing transactions, the recipients of which are mostly territorial tax authorities, business interests are also taken into account. A separate place is occupied by tax reconstruction – a mechanism in demand and expected by the market for determining the real size of the tax liability. There are subtleties in its application: if the company admits that it has received the performance of the obligation not from the party specified in the contract, but the transaction is real, expenses and deductions will be determined according to the documents from the actual contractor. The taxpayer himself must collect and submit them.

The taxpayer himself must collect and submit them.

An unrealistic transaction – if the goods have never been delivered or work has not been performed – in any case cannot be accepted in tax accounting and reconstructed. The problem of reconstruction is also revealed in connection with the opposition to the fragmentation of business through special tax regimes. The amounts of taxes paid, which were often not deducted by the tax authorities from the final amount of additional assessments, should reduce the tax liability.

Particular attention is paid to the prudence of taxpayers. The FTS assumes that the commercial prudence that companies exercise to assess the solvency of partners and the risk of default is identical to the prudence for tax purposes.

Innovations take into account the interests of business

Separately, the Federal Tax Service explained how it is possible to assess the availability of resources for the counterparty to fulfill obligations and determine whether it falls under the definition of a technical company.

It is recommended to request documents from potential partners and conduct their own verification both to eliminate the risk of being charged with a fine and to retain the ability to recover tax losses from a counterparty that misled the taxpayer about the fact of fulfillment of obligations to the budget.

The economic meaning of the transaction and its business purpose are also examined. The form of the transaction must correspond to the content, and the main motive for its completion cannot be tax. At the same time, the presence of a business goal in a series of transactions does not mean that this feature is inherent in each transaction. The tax authority will investigate the underlying motive of transactions individually.

Another block of explanations by the Federal Tax Service concerns the consequences of detecting defects in primary documentation for conscientious taxpayers. In tax disputes, the question often arose of how legitimate it is to refuse deductions and expenses if the document is signed by an unidentified person.